Post-Election Financial Planning: Strategies Million-Dollar IRA Owners Can Implement Now to Protect & Build Their Retirement Nest Eggs for 2025 and Beyond

Webinars are for high-net-worth individuals seeking to optimize their retirement and estate planning strategies in an ever-changing economic and political landscape.

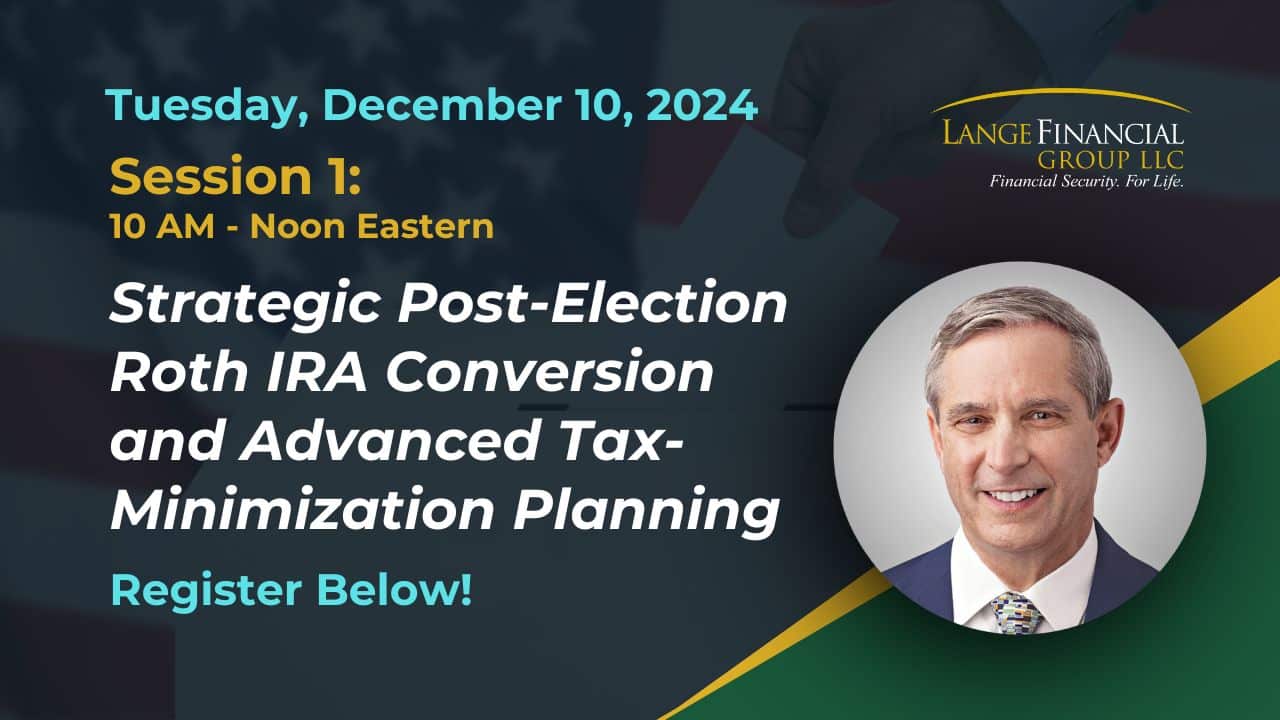

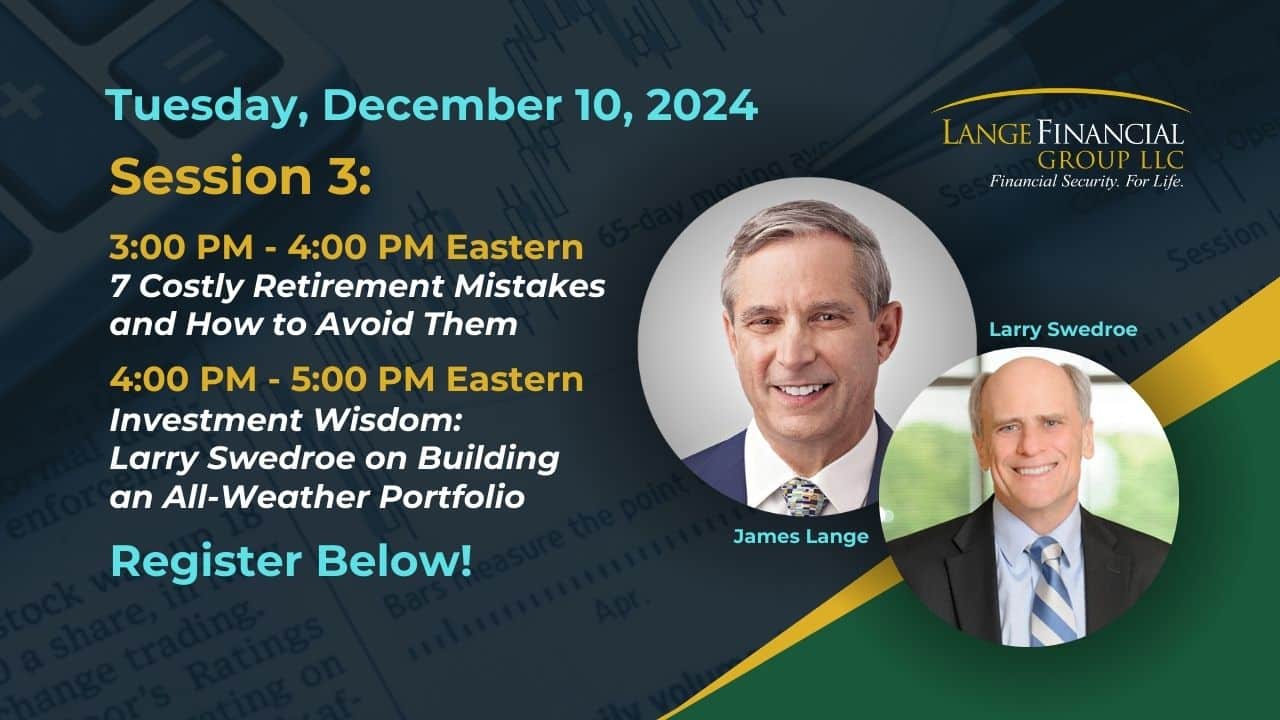

Tuesday, December 10, 2024

Register to attend 1, 2, or all 3 Free Webinars below.

If you are married, both spouses are encouraged to attend.

Empower Yourself and Seize New Opportunities to Secure Your Family’s Financial Future in These Uncertain Times

Major changes are anticipated across all spheres of American life, and it's entirely understandable to be concerned about how the election results could affect your long-term financial planning. The most pressing question on the personal financial planning side being: Should you alter or adjust your current retirement and estate planning strategies in response?

Our upcoming workshops will blend our developing electoral outcome-based recommendations with strategic advice we'd offer regardless. The descriptions for Sessions 1 and 2 outline some of the information that will almost certainly be covered.

Session #1: 10 am – Noon Eastern

Strategic Post-Election Roth IRA Conversion and Advanced Tax-Minimization Planning

Income Tax Policy: Navigating Potential Tax Increases

The impending sunset of the Tax Cuts and Jobs Act (TCJA) of 1997 is effective January 1, 2026. This means that, unless Congress acts, income tax rates will revert to higher 2017 levels. This shift could significantly impact your financial well-being going forward.

In this session, we’ll introduce you to battle-tested, proven retirement planning strategies that work, with a special emphasis on Roth IRA conversions.

You'll discover:

- Proactive Multi-Year Tax Planning: How to develop the ideal long-term Roth IRA conversion plan.

- Prepare for potential tax rate volatility.

- Asset Diversification for Tax Optimization: How to move a portion of your taxable investments (IRAs and other retirement plans) into tax-free environments of not only your Roth accounts, but 529 plans and your children's Roth IRAs and Roth 401(s). Note: This shift could potentially be more valuable to your children than making Roth IRA conversions directly in your own accounts.

Foundational & Advanced Roth Conversion Techniques including:

- Optimal Timing for Roth Conversions: The peer-reviewed math behind the best timing strategies.

- The Back-Door Roth IRA: How to contribute to a Roth IRA even if you exceed income limits.

- Benefiting from SECURE Act 2.0: How individuals born between 1951 and 1959 can profit from recent legislative changes.

- Tax-Free Transitions: How to convert after-tax dollars in retirement plans to a Roth IRA at no cost, potentially saving hundreds of thousands in taxes down the road.

- Inherited IRA Strategies: How to convert an inherited retirement plan to a Roth at your beneficiary’s tax rate after you die—a little-known strategy with big tax savings for those who qualify.

- Capitalizing Before Tax Rates Increase: The benefits of converting traditional IRA dollars into a Roth IRA before the 2026 scheduled sunsetting of the TCJA, locking in today's lower rates and enjoying tax-free withdrawals in the future.

Session #2: 12:30 – 2:30 PM Eastern

Post-Election Optimal Estate Planning for Married IRA Owners

Estate Planning Strategies: Preserving Your Legacy

Estate planning involves not only potentially saving estate and inheritance taxes, but also the far more likely problem: income taxes.

You see, the potential reduction of the federal estate and gift tax exemption in 2026—from $13.61 million to $7 million per person—could significantly impact high-net-worth families.

Many middle- and higher-income taxpayers will get clobbered with more income taxes at death, too.

You'll learn:

- Lifetime Gifting Strategies: How increasing lifetime gifts to your heirs now can reduce future tax burdens and provide financial assistance when it's most impactful for your loved ones. This approach isn't just about tax savings; it's also about enriching your family's lives today.

- Who Gets What? Strategy: A rarely discussed method that evaluates the tax consequences of leaving differing types of assets to children in different tax brackets. We will cover a similar strategy for charitable giving. By optimizing your strategies, you could save hundreds of thousands of dollars in taxes.

- State-Level Tax Considerations: Techniques to protect your wealth from potential increases in state-level income taxes, as well as inheritance and estate taxes. State taxes can significantly impact the assets your heirs receive, so proactive planning is essential.

Social Security: Maximizing Your Lifetime Benefits including:

- Risk and Reward Delaying Benefits: Are the risks of benefits cuts and dying young sufficient to take Social Security before 70 for the primary wage earner? And if you take Social Security before 70, can you stop it? Or should you delay taking your Social Security benefits to significantly increase your lifetime payouts, potentially by hundreds of thousands of dollars?

- Integrating Social Security into Your Retirement Plan: Strategies to incorporate Social Security strategy impact other areas of your planning. Learn how synergistically timing your Social Security benefits and Roth conversions can enhance your financial security.

Session #3: 3 – 5 PM Eastern

7 Costly Retirement Mistakes to Avoid + Exclusive Post-Election Investment Q&A w/ Larry Swedroe

3:00 PM – 4:00 PM

Join CPA/Attorney James Lange as he highlights common retirement planning mistakes that can undermine your financial security and legacy.

Key topics include:

- Mistake 1: Letting Lifelong Saving Habits Hinder Your Retirement

Accumulating wealth is important, but continuing to save without a plan can lead to:

- Missing out on rewarding experiences and family time

- Lost opportunities to assist heirs when they need it most

- Unnecessary tax burdens for your beneficiaries

Learn how to balance saving and spending to make the most of your wealth during your lifetime and ensure a favorable financial legacy.

- Mistake 2: Overlooking Discrepancies Between Your Will and IRA Beneficiary Designations

Did you know that the beneficiary designations on your IRA and retirement accounts override the instructions in your will or trust? Failing to align these can result in assets going to unintended recipients. Discover steps to ensure your retirement assets are passed on according to your true intentions.

4:00 PM – 5:00 PM

Exclusive Q&A with Larry Swedroe: Your Post-Election Investment Questions Answered

Please join renowned investment expert Larry Swedroe for a special 1-hour Q&A session to address your post-election investment questions.

Jim Lange will kick off the session with a timely question: "Larry, now that we know the outcome of the election and have some indication of the cabinet members the President-elect wants to appoint, what, if anything, should investors do differently?"

Submit Your Questions in Advance:

While we will take some questions live, we anticipate high demand and encourage you to submit your questions for Larry now at PayTaxesLater.com/Questions and Larry will answer your questions live on December 10th.

Don't miss this opportunity to gain valuable insights into retirement planning and post-election investment strategies from two leading experts. Register now to secure your spot!

Reserve your virtual seat today for these timely and informative webinars on:

Tuesday, December 10, 2024

Register to attend 1, 2, or all 3 Free Workshops below.

6 Valuable Bonus Gifts: Yours FREE When You Attend Any Session!

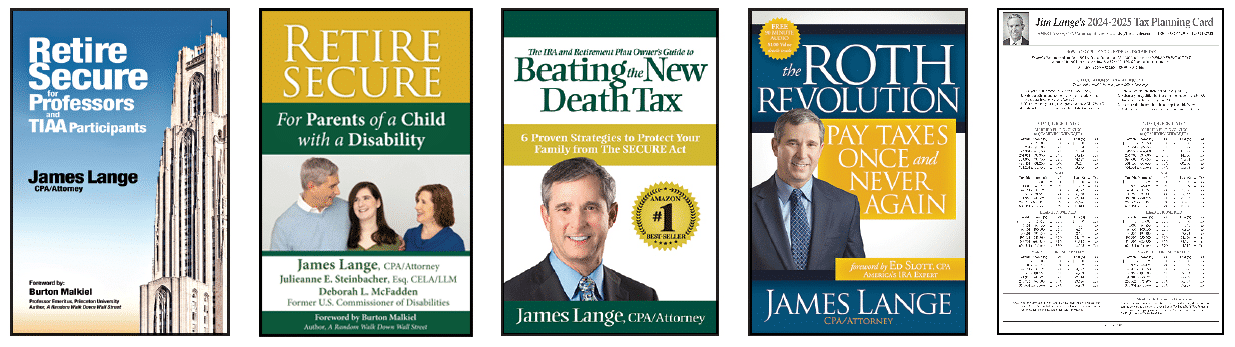

Bonus 1: Register today and you will receive a free hardcover copy of Jim’s magnum opus, Retire Secure for Professors and TIAA Participants, the best book Jim and his team have ever written. Please note 90% of the content is for all IRA and retirement plan owners. The book enjoys 80 glowing testimonials on Amazon.

Bonus 2: Your next gift is a digital copy of Jim’s best-selling book, Retirement Plan Owner’s Guide to Beating the New Death Tax, detailing how to respond to the SECURE Act.

Bonus 3: You will receive a digital copy of Jim’s 276-page best-seller, The Roth Revolution: Pay Taxes Once and Never Again. Jim shows how to use a series of Roth IRA conversions to grow income from your IRAs tax-free.

Bonus 4: You will receive a digital copy of our 2024-2025 Tax Planning Card.

Bonus 5: Attendees will also receive a digital copy of Jim’s brand-new book, Retire Secure for Parents of a Child with a Disability.

Bonus 6: Qualified attendees are eligible for a FREE Retire Secure Initial Consultation with Jim Lange and one of his number-crunching CPAs.

About James Lange, CPA/Attorney

Jim Lange’s tax and estate planning strategies have been endorsed by The Wall Street Journal (36 times). He has authored 10 best-selling books. A well-known Roth IRA expert, Jim authored the first peer-reviewed article on Roth IRAs in 1998 which was published in AICPA’s journal, The Tax Adviser. He has authored five peer-reviewed articles in Trusts & Estates, and he is a regular contributor for Forbes.com.

Some of Jim’s books have become classics endorsed by the country’s top experts. Retire Secure! was endorsed by Charles Schwab, Larry King, Jane Bryant Quinn, and 50 other experts; The Roth Revolution, endorsed by Ed Slott and Robert S. Keebler; The $214,000 Mistake, How to Double Your Social Security and Maximize Your IRAs, endorsed by Larry Kotlikoff, Jonathan Clements, and Paul Merriman; The Retirement Plan Owner’s Guide to Beating the New Death Tax, endorsed by Burton Malkiel and Larry Swedroe; Retire Secure for Professors and TIAA Participants, endorsed by Roger Ibbotson and Stephan R. Leimberg, Esq.; and Retire Secure for Parents of a Child with a Disability endorsed by Tatyana McFadden and James M. Dahle, MD.

Disclaimer: Lange Accounting Group, LLC offers guidance on retirement plan distribution strategies, tax reduction, Roth IRA conversions, saving and spending strategies, optimized Social Security strategies, and gifting plans. Although we bring our knowledge and expertise in estate planning to our recommendations, all recommendations are offered in our capacity as CPAs. We will, however, potentially make recommendations that clients could have a licensed estate attorney implement.

Asset location, asset allocation, and low-cost enhanced index funds are provided by the investment firms with whom Lange Financial Group, LLC is affiliated. This would be offered in our role as an investment advisor representative and not as an attorney.

Lange Financial Group, LLC, is a registered investment advisory firm registered with the Commonwealth of Pennsylvania Department of Banking, Harrisburg, PA. In addition, the firm is registered as a registered investment advisory firm in the states of AZ, FL, NY, OH, and VA. Lange Financial Group, LLC may not provide investment advisory services to any residents of states in which the firm does not maintain an investment advisory registration. Past performance is no guarantee of future results. All investing involves risk, including the potential for loss of principal. There is no guarantee that any strategy will be successful. Indexes are not available for direct investment. If you qualify for a free consultation with Jim and attend a meeting, there are two services he and his firms have the potential to offer you. Lange Accounting Group, LLC could offer a one-time fee-for-service Financial Masterplan. Under the auspices of Lange Financial Group, LLC, you could potentially enter into an assets-under-management arrangement with one of Lange’s joint venture partners.

Please note that if you engage Lange Accounting Group, LLC and/or Lange Financial Group, LLC for either our Financial Masterplan service or our assets-under-management arrangement, there is no attorney/client relationship in this advisory context.

Although Jim will bring his knowledge and expertise in estate planning to this workshop and to the meetings, it will be conducted in his capacity as a financial planning professional and not as an attorney. This is not a solicitation for legal services.