Table of Contents

Reprinted with permission from Forbes.com where Jim is a regular contributor.

SECURE 2.0 improves Roth retirement options, including allowing employer matching contributions direct to a Roth retirement plan and delays Required Minimum Distributions (RMDs) for many.

On December 29, 2022, as part of the omnibus spending bill, President Biden signed into law the SECURE 2.0 Act of 2022 (SECURE 2.0). The law contains significant changes to employer-provided retirement plans and individual retirement plans and has particularly meaningful changes for Roth accounts. I colorfully described the original SECURE Act of 2019 as a stinking pig wrapped in ribbon (primarily due to the death of the stretch IRA), but SECURE 2.0 actually lives up to its name. It provides significant savings enhancements for retirement planning and allows for increased Roth contributions and conversion opportunities including:

- Match and Nonelective Contributions Can Now Be Roth

- Roth SIMPLE and SEP IRAs

- Student Loan Matching Contributions Permitted

- No More Roth 401(k) RMDs

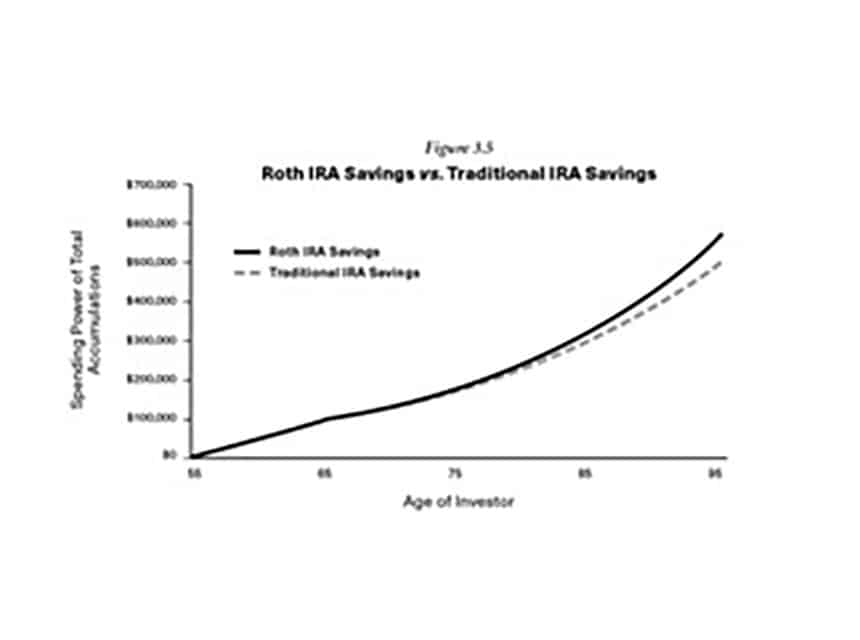

I have long been a proponent of Roth IRAs and SECURE 2.0 will allow many more Roth saving options, which I will highlight below. As I have written before, the Roth IRA (or work Roth retirement plan) is superior, in most cases, to the deductible IRA (or work traditional retirement plan). And depending on the investment period and your current and future tax brackets, even making the most conservative of assumptions, the Roth IRA will often provide more purchasing power than a traditional deductible IRA. See Figure 3.5 below.

Assumptions for Figure 3.5: Roth IRA Savings vs. Traditional IRA Savings

- Contributions to a Roth IRA are made in the amount of $7,000 per year, beginning in 2022, for a 55-year-old investor, for 11 years until he reaches age 65.

- Contributions to a regular deductible IRA are made in the amount of $7,000 per year by a different 55-year-old investor, for 11 years until he reaches age 65. This investor’s IRA contribution creates an income tax deduction for him of 24 percent, or $1,680. I will give the best-case scenario and say that this investor did not spend his tax savings. Instead, he invested his tax savings into his after-tax investment account and did not spend it.

- The investment rates of return on the Traditional IRA, the Roth IRA and the after-tax investment accounts are all 6 percent per year.

- For the after-tax monies, the rate of return includes 70 percent capital appreciation, a 15 percent portfolio turnover rate (such that much of the appreciation is not immediately taxed), 15 percent dividends, and 15 percent ordinary interest income.

- Ordinary income tax rates are 24 percent for all years.

- Tax rates on realized capital gains are 15 percent.

- Beginning at age 72, the RMDs from the Traditional IRA are reinvested into the after-tax savings account.

- The balances reflected in the figures reflect spending power, which is net of an income tax allowance of 24 percent on the remaining Traditional IRA balance. If the full amount was actually withdrawn in one year, however, the tax bracket may be even higher and make the Roth IRA appear more favorable.

Employees and Employers, Take Notice

The first huge change for people who are still working is that employers will now be able to provide employees with the option to receive matching and nonelective contributions to a Roth account for their 401(k)/403(b)/457(b) plans. Under prior law, all employer contributions had to be deposited to a traditional account (pre-tax), not a Roth—employees could choose a Roth account for their contribution, but the employer could not.

This is an optional provision for employers. Employers must change their plan documents to provide this option. Employees won’t have this option immediately unless their employer has changed their plan offerings since the beginning of the year. Employers are not required to provide the options.

One of the purposes of this article is to not only educate employees, but also to encourage all employers, both in the for-profit and not-for-profit worlds, to amend their plans immediately. In most cases, every month employers delay amending their plan, it is hurting their employees. Plan documents without this vital plan amendment will limit valuable options for employees to save for their retirement in the most effective manner. Plus, this additional feature comes at no cost to the employer.

All taxes on Roth contributions will be the employee’s responsibility and the match will be immediately vested. Almost all younger workers should take advantage of this provision and most mid and even some late-career employees should also.

I had the pleasure of interviewing Burton Malkiel earlier this year and he kept stressing the importance of regular Roth contributions, especially for younger workers. Systematic contributions to a retirement plan act like dollar cost averaging and doing it with Roths is usually more effective than with traditional contributions. Again, while this provision is effective for 2023, employees will not have the option if their employer has not updated plan documents and payroll systems.

We are updating our 401(k) at Lange to allow our employees to take advantage of this option, and I hope all employers do the same.

It is understood that if your employer offers matching contributions for your retirement plan, you should contribute at least the amount necessary to receive the full amount that the employer is willing to match. Both under the old law and under the new law, the employee’s contribution can be to a Roth or a traditional account. After you pay the taxes on a Roth matching contribution, it will grow income-tax-free with no taxes due when the money is withdrawn. Traditional contributions will be made on a pre-tax basis, and taxes will be owed when the money is withdrawn.

The employer match provides an immediate positive return on your investment and is the easiest way to maximize your retirement savings. It is a win-win scenario.

For employees who want to contribute the most possible, allow me to frame the “Roth versus a traditional contribution” scenarios. Let’s assume the employer has a 50% match policy and the employee contributes $30,000 per year in 2023 ($22,500 maximum plus the $7,500 catch-up if age 50 or older).

The employer’s contribution would be $15,000. If the employer’s contribution goes to the traditional portion of the plan, the employee, in effect, receives $10,000 in immediate purchasing power because of the 33% income tax liability when the funds are withdrawn. If the employer’s share goes to the Roth, then the employee is receiving $15,000. The employee will need to pay the tax on the contribution—he can’t deduct the contribution—but in effect, the contribution is $5,000 higher when measured in purchasing power, not including the income-tax-free growth on the contribution.

SEPS and SIMPLEs

SECURE 2.0 also expands the opportunity for some employees to save to a Roth account. One such opportunity, starting in 2023, is to allow employee contributions to SIMPLE and SEP IRAs to be Roth and in an analogous manner, employees are also allowed (if offered by the plan) to treat their employer SEP contributions as Roth. I usually prefer a 401(k) plan to a SIMPLE or SEP, but still, welcome the change.

Student Loan Match

Starting in 2024, employers will be permitted to offer matching contributions for employees who are paying off student loans without additional contributions from the employee. Under these circumstances, the employer match can be based on the qualified employee student loan payments—it will be as if the loan payments were elective deferrals into the plan. Again, it is up to the employer to allow this option, but it would be a huge benefit to help an employee who participates in an available employer match who would otherwise not be saved. It is very imaginable that these individuals might feel overwhelmed by the debt and unable to mark additional money to save for retirement. On the other hand, this will cost an employer money if they choose to add this option to their retirement plan.

No RMD for Roth 401(k)s and Roth 403(b)s

Finally, starting in 2024, SECURE 2.0 aligns employer-sponsored Roth plans with Roth IRAs and now the employer plans will also be exempt from the RMD requirements (just as Roth IRAs are) while the participant is alive. This avoids the extra effort and hassle of rolling over a 401(k) or 403(b) to a Roth IRA just to avoid the RMD. The process will be much simpler and not force an employee out of an employer plan who otherwise may want to remain.

Increased Age for RMDs (and Additional Time for Roth Planning)

Currently, the age for RMDs is 72 (before the SECURE Act, the RMD age was 70½). Under SECURE 2.0, the ages for RMDs change again:

- If you were born before 1950, RMDs started at age 70½

- If you were born in 1950, RMDs start at age 72

- If you were born between 1951 and 1959, RMDs start at age 73

- If you were born in 1960 or later, RMDs start at age 75

Note: There is a discrepancy within the bill that needs to be corrected. For those individuals born in 1959, the bill inadvertently reads that they have two ages to begin taking their RMDs: age 74 and 75. The table above reflects how experts perceive the intention of the bill. Stay tuned for a technical amendment in the future. For some, you will now have an extra three (3) years for additional planning considerations, including accelerating more Roth conversions and/or smoothing out Roth conversions over a period of time to lower Income Related Monthly Adjusted Amount (IRMAA) for Medicare charges, net investment income taxes, and possibly, capital gains tax brackets.

The important part about the increased age for RMDs from a Roth conversion standpoint, is obviously there will be a longer window to make lower-cost Roth IRA conversions.

In conclusion, employers please update your documents to better serve your employees. For people still working, assuming that Roth accumulations make sense for you when your employer does offer the Roth option for the employer portion, strongly consider taking advantage of it.

Tax-Savvy IRA Owners Should Celebrate Passage of SECURE Act 2.0

Learn About New Opportunities for Million-Dollar IRA Owners

Three FREE Educational Webinars:

Tuesday, February 21, 2023

Finally, some good news coming from Congress, but only for those who learn how to take advantage of the ground-breaking legislation.

Do yourself and your family a huge favor and attend these workshops.

Secure Act 2.0 provides new tools and opportunities for IRA owners to implement optimized strategies to get the most out of what they’ve got. Don’t be complacent. Be proactive. Education and action are the keys to increasing and preserving your retirement wealth!

Our team is committed to helping IRA owners save more, spend more, and leave more. Our new and classic strategies—including some advanced techniques that are not well-known or used—are much more powerful with the new legislation. Equally exciting, strategies that we thought would be eliminated are still permitted which means more tax-free contributions for many viewers.

We also wanted you to hear from not only Jim but some of the top people on our team. We will be expanding our webinar panel of experts to include Matt Schwartz, our veteran quantitative estate attorney, and two of our number-crunching CPAs, Steve Kohman and Jen Hall. This critical-thinking team will analyze the offerings and opportunities in SECURE Act 2.0.

Join us to discover both proven and new methods for getting the most from your IRAs and retirement plans.

Presenters Include:

• Jim Lange, CPA/Attorney, eight-time best-selling author with 36 appearances in The Wall Street Journal.

• Matt Schwartz, Estate Attorney, will share proactive legal techniques he routinely uses to implement estate planning essentials.

• Steve Kohman, CPA, CSEP®, CSRP®, will share critical nuances on Roth IRA conversion optimization.

• Jen Hall, CPA, CMA, CFP®, CRPC®, will share her process for “running the numbers.”

You must register for each session individually.

Webinar 1: 11:00 AM – 1:00 PM (Eastern)

Navigating SECURE Act 2.0: New Opportunities for

Million-Dollar IRA Owners

(Presenters: Jim Lange, Steve Kohman Matt Schwartz, Jen Hall)

Click here to register

In this session, we will cover:

• How many can profit from delayed RMD beginning dates.

• Implications of new rules allowing employers to offer Roth contributions.

• Expanding opportunities to move from the taxable to the tax-free investing environment—potentially more valuable than Roth IRA conversions for some investors.

• New opportunities to transition after-tax dollars of retirement plans, to a Roth IRA at no cost —potentially saving hundreds of thousands of dollars in taxes down the road.

• How to benefit from back door and Mega back door Roth IRA conversions that we thought would be eliminated.

• Capitalizing on Roth IRA conversions through 2025 while favorable income tax rates remain and before 2026 when the “Sunset Provisions” of The Tax Cut and Jobs Act of 2017 take effect and tax rates go up substantially.

• How to plan for the conversion of an inherited retirement plan to a Roth at your beneficiary’s tax rate, not your own.

• Rollover possibilities of 529 plans to Roth IRAs making 529 plans more attractive than ever.

Webinar 2: 1:30 – 3:30 PM (Eastern)

The Best and Most Flexible Estate Plan for Retirement Plan Owners

(Presenters: Jim Lange and Matt Schwartz)

Click here to register

Getting your retirement plan correct is critical, but if you don’t get your estate planning right, your family could lose hundreds of thousands in taxes. That can be prevented.

Between the SECURE Act and pending tax hikes, unless you take aggressive action, you and your loved ones will likely take a massive income tax hit on the monies in your IRAs and retirement plans. This workshop will concentrate on what you can do to protect your estate from Uncle Sam.

We will review what we consider the best estate plan for most married IRA owners but will also cover some advanced trust planning. For many $1M+ IRA or retirement plan owners, unless you take aggressive action, your loved ones will likely take a massive income tax hit on the monies in those plans…

Getting trusts right, particularly when the underlying asset is an IRA or retirement plan is crucial. In our reviews of trusts of this type, more than half the trusts we examine are not done right. This common estate planning mistake can be devastating for families with a large IRA and who prefer leaving money to one or more beneficiaries in a trust rather than leaving it to them outright. This could be a minor’s trust, a spendthrift trust, or an asset protection trust. This webinar shines a light on this common sloppy and costly estate planning error and how you can get it right.

In this session, we will also dive into:

• The details of the best estate plan for married retirement plan owners known as Lange’s Cascading Beneficiary Plan.

• Should your heirs inherit your IRA and other retirement assets directly, or would naming a trust be wiser?

• Do you need the ever more popular “I don’t want my no-good son-in-law to inherit one red cent of my money trust?”

• We will combine our newest thinking with some of our classic strategies for protecting your children or grandchildren from themselves, but also creditors, possibly including their spouse.

Webinar 3: 4:00 – 5:00 PM (Eastern)

A Live Q&A with Jim Lange and Other Team Members

Click here to register

Fielding Your Questions about the SECURE Act 2.0., IRAs, 401(k)s, Roth Conversions, Tax Minimization, Estate Planning, and More

We will answer attendees’ questions submitted in advance of these webinars as well as those submitted during the webinar. Take advantage of this remarkable opportunity to have your financial questions answered.

You must register for each session individually.

Register to Attend 1, 2, or all 3 FREE Webinars at:

https://PayTaxesLater.com/Webinars

Investment advisory services are provided through Lange Financial Group, LLC. Past performance is no guarantee of future results. All investing involves risk, including the potential for loss of principal. There is no guarantee that any strategy will be successful. Indexes are not available for direct investment.