Table of Contents

- My Well-Diversified Portfolio Underperformed the S&P Last Year

- Would You Do Me and Your Friends/Colleagues This Important Favor?

- One-on-One Training Done Right

My Well-Diversified Portfolio Underperformed the S&P Last Year

Should I Abandon Value Stocks?

Value stocks underperformed growth stocks by a material margin in the U.S. last year. However, the recent negative value premium was not unprecedented. Measured by the difference between the Russell 1000 Growth and Russell 1000 Value indices, value stocks delivered the weakest relative performance in seven years.

We suspect at least a few investors with value-tilted portfolios will find these results discouraging and may contemplate abandoning value stocks.

Total Return for 12 Months, Ending December 31st 2015

| Russell 1000 Growth Index | 5.67% |

| Russell 1000 Value Index | -3.83% |

| Value minus Growth | -9.49% |

Let’s review a previous period when value strategies underperformed to gain some perspective.

As many growth stocks and technology-related firms soared in value in the 1990s, value delivered positive returns but fell far behind in the relative performance race. By the end of 1998, value stocks had underperformed growth stocks over the previous 1, 3, 5, 10, 15, and 20 years. The inception of the Russell indices was January 1979, so all the available data (20 years) from the most widely followed benchmarks indicated superior performance for growth stocks. To some investors, it seemed foolish for money managers to hold “old economy” stocks like Caterpillar (-3.1 percent total return for 1998) while “new economy” stocks like Yahoo! Inc. appeared to be the wave of the future (743 percent total return for 1998).

Many value-oriented managers counseled patience, but for them, the worst was yet to come. In 1999, growth stocks shone even brighter as value trailed by the largest calendar year margin in the history of the Russell indices — over 25 percent.

Total Return for 1999

| Russell 1000 Growth Index | 33.16% |

| Russell 1000 Value Index | 7.36% |

| Value minus Growth | -25.80% |

In the first quarter of 2000, growth stocks streaked to a 7 percent return while value stocks returned only 0.48 percent. As of March 31st 2000, value stocks had underperformed growth stocks by 5.61 percent per year for the previous 10 years and by 1.49 percent per year since the inception of the Russell indices in 1979. A Wall Street Journal article appearing in January profiled a prominent value-oriented fund manager who received angry messages; his shareholders ridiculed him for avoiding technology investments. Two months later he was replaced amidst persistent shareholder redemptio dns.

With value stocks falling so far behind in the performance race, it seemed plausible that value would need a lifetime to catch up.

It took less than a year.

By November 2000, value stocks had delivered modestly higher returns than growth stocks since index inception (21 years, 11 months). By the end of February 2001, value stocks had outperformed growth over the previous 1, 3, 5, 10, and 20 years and since-inception periods.

The reversal was dramatic. Over the period April 2000 to November, value stocks outperformed growth stocks by 26.7 percent and by 39.7 percent from April 2000 to February 2001.

This type of result is not confined to the technology boom-and-bust experience of the late 1990s. Although less pronounced, a similar reversal took place following a lengthy period of value stock underperformance ending in December 1991.

The moral of the story?

Prices are difficult to predict and dramatic changes in relative performance can take place in a short period of time.

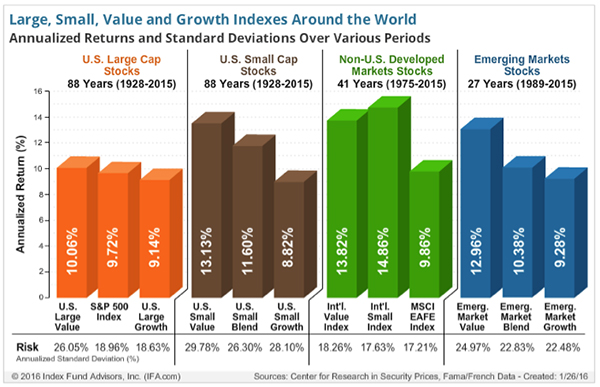

While there is a sound economic rationale and empirical evidence to support our expectation that value stocks will outperform growth stocks and small caps will outperform large caps over longer periods, we know that value and small caps can underperform over any given period. Results from previous periods reinforce the importance of discipline in pursuing these premiums. –Weston Wellington

Value is still a good bet.

In 2015 growth significantly outperformed value across large, small, and mid-caps and all value styles underperformed the S&P 500. So it’s reasonable that you may have seen a dip in your well-diversified portfolio. However, from 2000-2015 small-caps and emerging markets outperformed the S&P 500, proving to be good portfolio diversifiers and value outperformed growth across all capitalizations.

2000-2015 annualized returns

| Russell 2000 (Small Cap) | +6.60% |

| MSCI EM (Emerging Market) | +5.90% |

| S&P 500 (Large Cap) | +4.10% |

| MSCI EAFE (Developed International) | +2.80% |

2000-2015 Value vs. Growth annualized returns

| S&P 500 Value (Large Value) | +4.75% |

| S&P 500 Growth (Large Growth) | +3.22% |

| Russell Mid Value (Mid Value) | +9.72% |

| Russell Mid Growth (Mid Growth) | +4.66% |

| Russell 2000 Value (Small Value) | +9.03% |

| Russell 2000 Growth (Small Growth) | +3.98% |

(Callan Periodic Table and the JPMorgan Guide to Markets and Asset Class Returns 2000-2015)

And while past performance does not indicate future results, the chart below indicates that between 1927 & 2013, value proves a strong performer.

The foregoing content reflects the opinions of Lange Financial Group, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct.

Past performance is not a guarantee of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns.

All investing involves risk. Asset allocation and diversification does not ensure a profit or protect against a loss.

Would You Do Me and Your Friends/Colleagues This Important Favor?

Have you ever had some information that was so valuable you wanted to tell as many people as you could? Maybe it was a bit of insight, an article, a story, or something else that would enhance the quality of life for your friends, colleagues, and perhaps even the world at large?

Have you ever had some information that was so valuable you wanted to tell as many people as you could? Maybe it was a bit of insight, an article, a story, or something else that would enhance the quality of life for your friends, colleagues, and perhaps even the world at large?

I have timely, life-changing information regarding the best strategies for retired married couples making decisions about Social Security. To add to the urgency, there is a deadline of April 29th 2016 for many couples to get this right. So, in addition to multiple radio shows, a special interview, and many workshops, I have now written a short book on how married couples who meet the qualifications can get Social Security right — as long as they act before the deadline of April 29th 2016.

If you are married and between the ages of 62 and 70 and have not discussed Social Security strategies with our office, I urge you to read my new mini-book, The Little Black Book of Social Security Secrets. You can request a hard copy from our office or go to www.paytaxeslater.com/ss.

If you have friends or colleagues who are married and between the ages of 62-70, I urge you to send them the link to the e-book version at www.paytaxeslater.com/ss. Tell them it is valuable information, with concrete recommendations, and a quickly approaching deadline.

If you or your friends would prefer to hear the information in person, please sign up to attend one of my two upcoming workshops on Social Security:

April 2nd 2016 at Crowne Plaza Pittsburgh South, starting at 9:30 a.m. or

April 9th 2016 at Courtyard by Marriott, Monroeville, starting at 9:30 a.m.

For more details, please see the back of the newsletter.

The book is short, easy to read, and includes graphs. Our entire office has worked quickly and whole-heartedly to get this out, and we all want to spread the word.

Decisions about Social Security frequently do not get the attention they require. A couple who takes Social Security too early, without thinking long-term, may be seriously compromising the financial security of the surviving spouse when the first spouse dies. And statistically, that is the wife. So, women, take note. This is a discussion you need to have with your husband and your financial advisor.

A smart Social Security strategy combined with Roth conversions can make a huge difference in how long your money lasts and how well you live into your old age. Here is a scenario:

There were two married couples, the Rushers and the Planners, with identical earnings records and investments. The Rushers didn’t take time to read this book and ended up running out of money. The Planners read this book, utilized the recommended strategies, and when the Rushers ran out of money, the Planners still had $2,013,881 left.

While the numbers for most couples will not be that high, they often will be measured in the hundreds of thousands of dollars if you get the Roth IRA conversion strategy and the Social Security strategy right.

I will send a hard copy of the book to anyone who asks — call the office at 412-521-2732 or email a request to admin@paytaxeslater.com. If you belong to an organization or church group with a newsletter, please feel free to reference our link to the e-book. Again, if someone contacts the office, we will send out a hard copy, and feel free to add that information to your newsletter too. We urge all married couples between the ages of 62 and 70 to read this mini-book.

Thank you in advance for this effort. It really means a lot to me.

Personal note:

In the December 2015 newsletter, I publicly committed to losing 15 pounds by March 31, 2016. As of February 26, 2016, I have lost 21 pounds and am at 185.8 lbs. I was at 206.8. My new goal is to get down to 180 pounds by March 31, 2016. I am already lighter than I have been in many years. Since my diet was already limited to no sugar, no gluten, very few grains, and no dairy, and I was exercising a fair amount, the only real opportunity to lose weight was portion control. To be honest, getting down to 180 pounds will be tough, but not nearly as tough as maintaining that weight. But, one step at a time. For now, I am focusing on getting down to 180 pounds.

One-on-One Training Done Right – Consider a Personal Trainer

Having a personal trainer has made an enormous difference in the quality of life for me and my wife, Cindy — and it probably can for you too. The health benefits of doing resistance training three days a week are considerable. When I broke my hip, the surgeon said I could go back to work half time a month after the surgery. I was back full time within a week of surgery. Though there were other factors, my physical condition before the accident was clearly the reason I recovered so well.

Having a personal trainer has made an enormous difference in the quality of life for me and my wife, Cindy — and it probably can for you too. The health benefits of doing resistance training three days a week are considerable. When I broke my hip, the surgeon said I could go back to work half time a month after the surgery. I was back full time within a week of surgery. Though there were other factors, my physical condition before the accident was clearly the reason I recovered so well.

As much as it was helpful, I used to only do weights sporadically. Then, I warmed up to the value of having a trainer. While obviously the quality of the trainer is important, for me it is the discipline of having three “business appointments” a week, and subject to rare exceptions, I keep my business appointments.

Our trainer comes to our house on Tuesday, Thursday, and Sunday. I work out from 8 a.m. to 9 a.m., and then Cindy trains from 9 a.m. to 10 a.m. We did make a little mini-gym out of our basement, but we have minimal equipment — none of those fancy weight machines that you find in a real gym. We do have an early “One Gym” model — the kind Chuck Norris advertises on TV. That is more than enough for a good trainer.

It is easy to roll out of bed, throw on exercise clothes, train, eat breakfast, shower, and then head off to work. It is so much more convenient than going to the JCC or Club One. I don’t have to drive there, work out, deal with social conversations that eat up extra time, or sacrifice privacy! Then, assuming I remember all my work clothes, toiletries, etc., I shower, get dressed, and drive to work.

For aerobic exercise, I do have a few machines at home, but since my leisure activities are hiking, biking, and kayaking, I tend to get adequate aerobic activity without gym equipment.

When I was single 23 years ago, the gym served a social purpose, but now I am more time-starved than socially-starved. You can decide for yourself if it is better to have someone come to your house or for you to go to a gym — the bottom line for me is still the discipline of a schedule.

Finding a trainer whose style fits with you and your objectives can take a bit of time. Their role cannot simply be filled by that one friend who knows how all the weight equipment in the gym works, or a co-worker who’ll chat with you as you jog on the treadmill. Those people make great workout buddies who can help you pass the time, but rarely will they help you achieve long-lasting results. Personal trainers are professionals with legitimate credentials.

Don’t be afraid to shop around for your personal trainer and ask for trial sessions. If you’re a member of a gym or the JCC or your local YMCA, ask for business cards and referrals. Your doctor can also recommend personal trainers.

So, if you think you are ready to invest in your health and find a personal trainer, we’ve compiled a few key things to consider before you hire a beefed-up meathead addicted to gym selfies.

A Personal Trainer Keeps You Safe:

You should definitely consult with your doctor before engaging in a fitness regimen. Once you know your body’s limits, your personal trainer can abide by those guidelines and develop a program that fits you. Good personal trainers are also backed by any number of nationally recognized organizations (National Academy of Sports Medicine, National Strength and Conditioning Association, etc.) that also certify them in CPR and first aid. A personal trainer should keep you safe beyond simply spotting you on the bench press.

A Personal Trainer Coaches:

Each personal trainer will have his or her own philosophy. Talk to your potential trainers about how they work, how they will make adjustments for you if you have particular constraints, and what their goals are for you. Make sure your fitness goals fit their world and vice versa. Not all people are compatible with a drill-sergeant — you need to find someone you are comfortable with. Your trainer is your partner. He or she is there to help you reach new levels of fitness by motivating you, coaching you, and encouraging you to expand what you think you can do. Coaching style matters.

A Personal Trainer Stays Professional:

The right personal trainer arrives on time and gives you his or her undivided attention. They should be courteous, professional, and have good communication skills. Mutual respect is essential, so you need to be ready to work as well, when your trainer arrives.

If I have even planted a seed that will get you thinking about a new way to approach your fitness training, I will be glad. I wish you good luck, and good health.