by Glenn Venturino, CPA and James Lange, CPA/Attorney

Table of Contents

- Very Big Picture

- Federal Individual Income Tax Rates for 2019

- Medicare Tax

- Capital Gains and Losses

- Zero Percent Tax on Long-Term Capital Gains

- Step-Up-In-Basis Rules

- Taxes on Social Security Income

- Estate and Gift Tax Opportunities

- Miscellaneous Year-End Tax Reduction Strategies

- Charitable Giving

- Inherited IRAs

- Instructions for Prepaying Your 2019 City of Pittsburgh and Allegheny County Real Estate Taxes

With year-end approaching, it is the time to take some final steps to lower your 2018 income tax bill. The 2017 Tax Cuts and Jobs Act (TCJA), a major overhaul of the tax code, was signed into law at the tail end of 2017 by President Trump. There are significant tax reform changes for both individuals and businesses. The new law introduced lower tax rate changes while eliminating many traditional tax deductions claimed by taxpayers on prior year tax returns. There are certain areas of change where tax professionals are still waiting for additional guidance from the IRS on its application. With many taxpayers no longer itemizing deductions additional focus should shift to AGI (adjusted gross income) tax planning. Let’s first examine the new tax environment with regards to itemized deductions.

Itemized Deductions: We now have a higher standard deduction allowance ($12,000 for individuals, $24,000 for married filing jointly, $26,600 if 65 or over). There are also new and significant limitations on what we may include for itemized deductions that will be examined below. For those who never itemized or were near the threshold, the increase in itemized deductions is favorable. For others who are used to itemizing, particularly if you pay a lot of money in real estate and state and local income taxes, the change in itemized deductions will hurt you.

Very Big Picture

Gaming the Standard Deduction allowance versus Itemizing Deductions.

The changes to Form Schedule A- Itemized Deductions will potentially affect many taxpayers. The elimination of certain traditional deductions on Schedule A will leave many taxpayers now claiming the higher standard deduction as its replacement. We can safely make this assumption due to the elimination and or reduction of traditional Schedule A items used by taxpayers in 2017 but no longer available in 2018. We will hit on some key areas affected and ideas to consider.

Bunching Strategy. Bunching your itemized deductions is a technique that involves accumulating deductions, so they are high in one year and low in the following year. If your tax deductions normally fall short of itemizing, or even if you can marginally itemize, you can benefit from the “bunching” strategy. It’s very typical for most taxpayers to wait until tax time to add everything up and use the higher of the standard deduction or their itemized deductions. It should be easier for most taxpayers to project their total itemized deductions before the end of 2018 due to the elimination of certain itemized deductions and limitations on others (SALT). By being proactive, you can time the payments of tax-deductible items to maximize your itemized deductions in one year while using the standard deduction the following year.

Medical Expenses. They will still be tax deductible in 2018 assuming you qualify in the first place. To be able to deduct medical expenses in 2018 your total out of pocket costs must exceed 7.5% of your adjusted gross income. This 7.5% windows closes at the end of 2018. What to do. If you don’t believe you’ll be able to itemize your deductions in 2019, then you should consider paying any last-minute medical expenses before December 31, 2018. Better used than lost. Another reason to consider paying any medical expenses before year end is the change in the rules for the 2019. Effective next year, the phaseout rate percentage increases to 10% once again. Be careful though, if there is dramatic difference in your adjusted gross income in either year determine which year the medical expense will reap the greater tax benefit.

State and Local Tax Deductions. The overall deductible limit for 2018 is limited to $10,000. This limit applies to a combined total that will include state and local income taxes, real estate taxes, sales tax, personal property tax etc. In our opinion, the deduction limitation of $10,000, will be the primary reason why more taxpayers will be using the 2018 standard deduction versus actual itemized deductions.

There is not a lot of wiggle room is this category. If you will be itemizing your deductions and you haven’t reached the $10,000 max threshold, some opportunity to prepay any state or local income tax may be considered.

Note – Taxpayers living in states (excluding Pa) who still itemize their federal deductions should review their state income tax return. There are state and local income tax addbacks on many state income tax returns. You may want to consider deducting all your real estate taxes paid and less of your state income taxes on Schedule A. At this point, we don’t know how states are going to handle the new law changes, so you may be able to work around it.

Charitable Donations. The theme here is similar. If you don’t think you’ll be itemizing your deductions in 2019, but will this year, consider making last minute cash and non-cash charity donations before year-end. If you don’t have the extra cash available today, you can use a credit card before year-end and still qualify for a 2018 tax deduction.

Bunching Charitable Donations. Consider bunching charitable donations every other year while taking the standard deduction in the off years. This strategy may be an effective way to receive a greater tax benefit from your charitable giving. Charities are very active with their solicitations during the holiday season and would be happy to receive gifts near year-end or early in the new year. If the gift is appreciated stock, the tax benefits are even greater.

One planning technique that may be more advantageous in 2018 and beyond is the use of Qualified Charitable Distributions. See the section titled “Charitable Giving” for details on using this strategy. A Helpful Tip. If you are currently using QCDs please make sure you receive acknowledge letters for any single donation of $250 or more from the charitable organizations before filing your tax return. The IRS requires the letter under the Substantiation and Disclosure requirements for the donation to be tax-deductible.

![]() ALERT. Especially important to seniors who no longer itemize their deductions. If your 2019 Required Minimum Distributions (RMDs) will come entirely from qualified plans such as 403(b)s and 401(k)s, consider an IRA rollover, or partial rollover, where applicable before December 31, 2018. You will not be eligible to take advantage of Qualified Charitable Distributions in 2019 unless this action is taken. Determine an IRA rollover amount that will create an RMD large enough to meet your charitable giving goal.

ALERT. Especially important to seniors who no longer itemize their deductions. If your 2019 Required Minimum Distributions (RMDs) will come entirely from qualified plans such as 403(b)s and 401(k)s, consider an IRA rollover, or partial rollover, where applicable before December 31, 2018. You will not be eligible to take advantage of Qualified Charitable Distributions in 2019 unless this action is taken. Determine an IRA rollover amount that will create an RMD large enough to meet your charitable giving goal.

Qualified Business Income Deduction for Business Owners. This is a real mess. The TCJA introduced a new ungodly complicated 20 percent tax deduction (also known as the Section 199A deduction) for eligible business owners such as sole proprietorships, LLCs, S Corporations, Partnerships and Trusts. The details of this deduction are beyond the scope of this letter. There are at least two books that I know of written just to explain this one new provision. Don’t let anyone tell you this was a tax simplification even if some things were simplified. There was long-awaited IRS guidance issued this past August, but many questions are still either unanswered or unclear. It is a valuable tax deduction for those who qualify. They will enjoy an extra reduction of taxable income without additional capital outlay. Certain deduction limits are imposed when taxable income exceeds threshold amounts. Keeping taxable income below these thresholds will preserve more of the qualifying deduction.

Defer Income and/or Accelerate Expenses. Many taxpayers don’t have much control in choosing whether to defer or accelerate income from year to year. However, the new tax law provides businesses and business owners, (including pass-through entities) with incentives and deductions to lower their overall tax costs. Being able to estimate income for 2019 can help with the decision of either accelerating income before the end of 2018 or deferring the income into 2019. The same is true for deductions. Try and use this flexibility to your advantage.

Tax Loss Harvesting. If your capital gains are larger than your losses, you might want to do some “loss harvesting.” This means selling certain investments that will generate a loss—converting them from unrealized losses to realized losses. You can use an unlimited amount of capital losses to offset capital gains. Large long-term capital gain income can often be the trigger that causes the Alternative Minimum Tax (AMT). This may be less likely to occur in 2018 due to certain positive changes in the TCJA as it relates to the AMT formula. For those higher-income taxpayers, lowering current year investment income by loss harvesting will generate even greater savings. These taxpayers can potentially lower the net investment income tax (the additional 3.8% tax) assessed on net investment income above certain levels.

Roth IRA Conversions. In general, we like Roth IRA conversions for taxpayers who can make a conversion and stay in the same tax bracket they are currently in and have the funds to pay for the Roth conversion from outside of the IRA. Unfortunately, the qualification “in general” is likely critically important. It is best to run the numbers to determine the most appropriate conversion amount for the current year and to plan for possible future conversions in your situation. We often develop a long-term Roth IRA conversion plan that usually involves multiple years of partial conversions.

Roth IRA Conversions. In general, we like Roth IRA conversions for taxpayers who can make a conversion and stay in the same tax bracket they are currently in and have the funds to pay for the Roth conversion from outside of the IRA. Unfortunately, the qualification “in general” is likely critically important. It is best to run the numbers to determine the most appropriate conversion amount for the current year and to plan for possible future conversions in your situation. We often develop a long-term Roth IRA conversion plan that usually involves multiple years of partial conversions.

The new tax has removed the ability for taxpayers to do any “recharacterizations” of Roth IRA conversions after 12/31/2017. The ability to “re-characterize” a Roth IRA back to a Traditional IRA was historically useful if the value of the Roth IRA had decreased since the conversion had taken place so you did not have to pay taxes on a larger amount of money if the value had gone down. Boo hoo. That was a fun strategy no longer available.

When a conversion plan is developed, we often recommend a conversion up to certain income limits to avoid additional Medicare premium cost increases or to avoid high rates of income tax on amounts of Roth conversion income over certain amounts.

In certain situations, utilizing a parent’s IRA and lower tax rates to do Roth conversions can be beneficial. The adult child (eventual beneficiary) can make a monetary gift to the parent to pay the tax on the conversion. Since the parent wouldn’t be receiving annual RMDs from the converted portion of the IRA, the child can make annual gifts to replace the lost income distributions to cover living expenses. Hold your breath while you wait for your child to make those gifts to you.

Going forward, Roth conversions under the new tax laws in 2018 may present a better opportunity to do conversions at the lower rates provided. The historical benefits of Roth IRAs and Roth conversions that grow in value have not changed. It is more important than ever to develop a Roth conversion plan considering your unique situation. If you are interested in this strategy, please contact us. Again, we refer you to the DVD we sent you, Unintended Benefits of Trump’s New Tax Law.

Modifications to Depreciation Limits on Luxury Automobiles. The annual depreciation limits have been expanded very generously for these business assets. If you’re in the market for a new business vehicle, consider the purchase before the end of 2018.

One of our main goals is to help clients identify specific opportunities that coordinate tax reduction with their investment portfolios. To achieve this goal, we continually stay current about potential year-end tax strategies and keep abreast of future strategies that our clients might want to consider to help reduce their taxes. We hope you are continually implementing long-term tax reduction strategies. We hope you will use us as a resource. We urge you to begin your final year-end tax planning now!

As a comprehensive financial services firm, Lange Financial Group, LLC is committed to helping our clients improve their long-term financial success. Of course, since every situation is different, not all strategies outlined will be appropriate for you. Please discuss all potential tax strategies with your tax preparer. Remember, this is not advice for preparing your taxes. Our goal is to identify ways to reduce your taxes!

My entire team at Lange Financial Group, LLC is available to provide you with updated information that can help with all your financial planning needs. If you would like us to send a copy of this important report to any of your friends or associates, please call Alice Davis at 412-521-2732.

It should be noted that our frequently-recommended three best tax shelters that create income-tax free growth are particularly appropriate in today’s tax environment. These three tax shelters are:

-

-

-

-

- Roth IRA conversions, please see my article, Roth: Four Little Letters Leading to Long-Term Financial Security at https://paytaxeslater.com/roth_ira.php.

- Section 529 plans (college plans for grandchildren and children). We would recommend Joe Hurley’s book, Saving for College or his website, savingforcollege.com.

- Life insurance.

-

-

-

As always, if you have any questions about your specific situation before our next scheduled meeting, please feel free to call your preparer.

Sincerely,

James Lange

Certified Public Accountant

Attorney at Law

![]() CAUTION: We are speaking in generalities, and it will be different for every taxpayer and we haven’t talked about the impact of Alternative Minimum Tax (AMT) which might offset some of the advantages that I’m talking about. Everybody really is a snowflake but I’m trying to give some guidance and some general principles that will help a lot, if not most, taxpayers.

CAUTION: We are speaking in generalities, and it will be different for every taxpayer and we haven’t talked about the impact of Alternative Minimum Tax (AMT) which might offset some of the advantages that I’m talking about. Everybody really is a snowflake but I’m trying to give some guidance and some general principles that will help a lot, if not most, taxpayers.

Here are the new rates for single and married filing jointly taxpayers.

Federal Individual Income Tax Rates for 2019

| Single Individuals | |

| Not over $9,700 | 10% of the taxable income |

| Over $9,701 but not over $39,475 | 12% of the excess over $9,701 |

| Over $39,476 but not over $84,200 | 22% of the excess over $39,476 |

| Over $84,201 but not over $160,725 | 24% of the excess over $84,201 |

| Over $160,726 but not over $204,100 | 32% of the excess over $160,726 |

| Over $204,101 but not over $510,300 | 35% of the excess over $204,101 |

| Over $510,301 | 37% of the excess over $501,301 |

| Married Individuals Filing Joint Returns and Surviving Spouses | |

| Not over $19,400 | 10% of the taxable income |

| Over $19,401 but not over $78,950 | 12% of the excess over $19,401 |

| Over $78,951 but not over $168,400 | 22% of the excess over $78,951 |

| Over $168,401 but not over $321,450 | 24% of the excess over $168,401 |

| Over $321,451 but not over $408,200 | 32% of the excess over $321,451 |

| Over $408,201 but not over $612,350 | 35% of the excess over $408,201 |

| Over $612,351 | 37% of the excess over $612,351 |

Medicare Tax

Once again in 2018, many higher-income taxpayers had larger tax bills due to the 3.8% Medicare contribution tax on net investment income. The focus must be on reducing your adjusted gross income to help mitigate the additional tax costs. Try and manage your adjusted gross income by keeping it as close to the threshold as possible. Going well below the threshold provides no additional benefit as it relates to computing the 3.8% surtax. With a few strategic moves, we might be able to reduce your adjusted gross income enough to mitigate the impact of these new taxes.

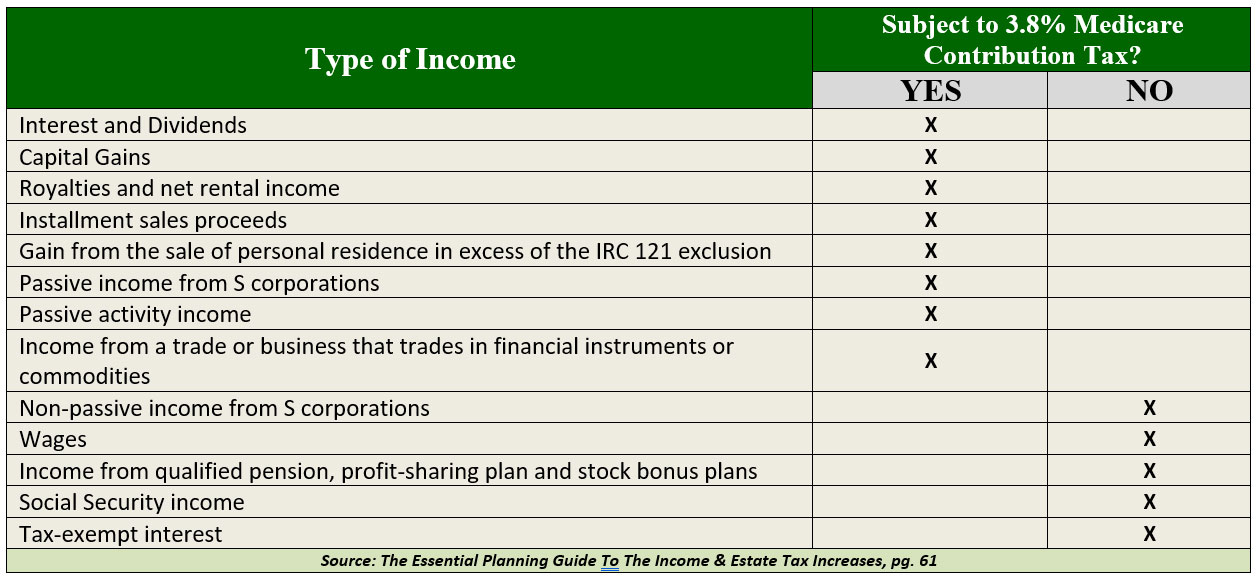

The Medicare contribution tax is imposed only on “net investment income” and only to the extent that total Modified Adjusted Gross Income (MAGI) exceeds $200,000 for single individuals and $250,000 for taxpayers filing joint returns. The amount subject to the tax is the lesser of:

-

- Net investment income; or

- The excess of MAGI over the applicable threshold amount listed above.

In addition to the complexity of calculating “net investment income” subject to the tax, another difficulty will be determining what constitutes net investment income that is subject to the tax. The chart below summarizes what qualifies as investment income under the new law.

Let’s examine ways to reduce your adjusted gross income before the end of 2018.

Many taxpayers, especially wage earners, have less control over their adjusted gross income when compared to self-employed taxpayers or even those in retirement. The following year-end moves can be ideal if any of these situations apply. If you have earned income from self-employment or an employee, one of the best ways to manage adjusted gross income is through retirement plan contributions. There are many alternatives to choose from that enable individuals to make retirement plan contributions. Now is an ideal time to make sure you maximize your retirement plan contributions for 2018, and start thinking about your strategy for 2019. Examine your year-to-date elective deferral contributions on your most recent pay stub. While your intentions may have been to maximize current year contributions to your 401(k) or 403(b), you may find out that you have not hit the maximum amounts as anticipated. There is still time to have your employer increase your contributions from your remaining paychecks to reach the maximum level of contributions allowable for 2018. Just recently the Internal Revenue Service announced cost‑of‑living adjustments affecting dollar limitations for pension plans and other retirement-related items for tax year 2019. Highlights include the following:

- Higher 401(k)/403(b) Contribution Limits. The elective deferral (contribution) limit for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan will be increased to $19,000. The catch-up contribution limit for employees age 50 and over who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan remains at $6,000. Looking ahead, if you’re currently set up to have the maximum salary deferral in 2018, you’ll need to increase it $500 for 2019.

- Planning Note: We are big proponents of using Roth 401(k) and Roth 403(b) plans for elective deferral contributions. Considering the current increased tax rate structure on certain investment income and the new section 199A for business owners an increased focus on reducing both adjusted gross and taxable income can be beneficial. Higher income taxpayers should consider switching back to making tax-deductible retirement plan contributions instead of funding their Roth accounts. An ideal strategy may be to split your contributions during the year if you’re in overlapping tax brackets. For example, consider making tax deductible contributions to reduce your income to the bottom level of your upper tax bracket and fund the remaining portion of your current year retirement account with non-deductible Roth contributions in a lower bracket. If you’re interested in this strategy, be sure to discuss with your professional tax preparer.

- Make a Tax-Deductible IRA Contribution. For those taxpayers who qualify, you can make a tax-deductible contribution of $5,500 with a catch-up (for taxpayers 50 or older) of an additional $1,000. The contribution can be made until April 15, 2019 and still be a deduction on your 2018 tax return.

- Planning Note: Due to the fact that the IRA contribution can be made after the end of the calendar year, calculating the actual tax savings provides a great advantage and shouldn’t be overlooked.

While it Lasts. For those of you who don’t qualify for a regular Roth IRA contribution (because your income is too high) and who have no other traditional IRAs, you can take advantage of a nice loophole in the code. Consider making a traditional IRA contribution and converting it immediately to a Roth IRA. You will run into complications with this strategy if you have other traditional IRAs. Once again, if this strategy fits your situation, make your 2018 contribution as soon as possible and repeat the process with your 2019 IRA contribution in early January 2019. If you are married, you can apply this strategy to your spouse even if they don’t work and assuming you have enough earned compensation to qualify.

Caution: If you are planning to do a rollover from a qualified plan to an IRA account prior to the end of the year, the above strategy will be unsuccessful, and the conversion will result in unexpected taxable income. It will not matter if the IRA contribution and the immediate Roth conversions occurred earlier in the year before the rollover date.

For those of you who can afford it, I encourage establishing and funding a Roth IRA for your children or even grandchildren and get a tax-free retirement fund started for their benefit. The longer period of tax-free growth provides a greater benefit. Like any IRA, the child or grandchild must have earned income to qualify for a contribution.

- Tax Loss Harvesting. If your capital gains are larger than your losses, you might want to do some “loss harvesting.” This means selling certain investments that will generate a loss—converting them from unrealized losses to realized losses. You can use an unlimited amount of capital losses to offset capital gains. However, you are limited to only $3,000 of net capital losses that can offset other income, such as interest, dividends and wages. Any remaining unused capital losses can be carried forward into future years indefinitely. Tax loss harvesting will generate even greater savings for higher income taxpayers that are subject to additional 3.8% net investment income tax on net capital gains. (Don’t forget to review your “Trust Investment Accounts” for loss harvesting as the higher tax rates apply at much lower levels of taxable income). Being tax savvy by reviewing your investment portfolio(s) for loss harvesting should be done annually prior to the end of the current tax year.

Please note that if you sell an investment with a loss and then buy it right back, the IRS disallows the deduction. The “wash sale” rule says you must wait at least 30 days before buying back the same security to be able to claim the original loss as a deduction. However, you can buy a similar security to immediately replace the one you sold—perhaps a stock in the same sector. This strategy allows you to maintain your general market position while capitalizing a tax break.

If you are planning to write-off a non-business bad debt, be sure to establish that it is bona fide debt and document unsuccessful efforts to collect. Form over substance matters in these instances.

-

- Utilize Installment Sales. If appropriate, reporting taxable gains using an installment sale will allow you to the spread the gain over several years rather than recognizing the entire gain in the year of sale. In many instances, this type of gain is also subject to the 3.8% Medicare surtax on “net investment income” thus managing your adjusted gross income can save additional taxes. Keep in mind that Medicare Part B premiums are determined by looking at your tax return from two years prior to the current year. An installment sale may enable you to spread the gain over several years while never crossing the threshold that would trigger increased Medicare premiums in any one year. Alternatively, if you have entered into an installment sale arrangement, you may have an option to elect out of the installment sales tax treatment. This election allows you to recognize the entire gain in the year of sale even though payments you receive will be over multiple tax years.

Consider this option if it’s the appropriate tax strategy.

Consider this option if it’s the appropriate tax strategy.

- Utilize Installment Sales. If appropriate, reporting taxable gains using an installment sale will allow you to the spread the gain over several years rather than recognizing the entire gain in the year of sale. In many instances, this type of gain is also subject to the 3.8% Medicare surtax on “net investment income” thus managing your adjusted gross income can save additional taxes. Keep in mind that Medicare Part B premiums are determined by looking at your tax return from two years prior to the current year. An installment sale may enable you to spread the gain over several years while never crossing the threshold that would trigger increased Medicare premiums in any one year. Alternatively, if you have entered into an installment sale arrangement, you may have an option to elect out of the installment sales tax treatment. This election allows you to recognize the entire gain in the year of sale even though payments you receive will be over multiple tax years.

-

- Maximize your HSA Contribution. If you are enrolled in an HSA (health savings account) plan, it is not too late to maximize your 2018 tax deductible contribution to the account. In fact, you have until April 15, 2019 to fund your HSA account and still get a 2018 tax deduction. Just like an IRA contribution, the exact amount of tax savings can be calculated. It is the only section in the Internal Revenue Code (the Triple Crown if you will) that allows a tax deduction on the way in, tax-free growth and tax-free qualifying distributions. For those who can afford it, fully funding the HSA account and never using the funds to pay for current medical expenses (using other monies to pay for medical expenses incurred) can allow for a big pot of tax-free money to accumulate over time to be used for future medical costs. These funds can come in handy during retirement when you normally experience more medical expenses while having less annual income. Also, once you reach age 65 you can use the money for reasons other than medical expenses. These distributions used for non-medical purposes will be penalty free but subject to income taxes. Sounds like an extra IRA account, without being subject RMD rules. Certainly not a bad thing to have.

- Funding Self-Employed Retirement Plans. If you are self-employed, you have other retirement savings options. We will review these alternatives with you when you come in for your appointment. One of my favorites for many one-person self-employed businesses is the one person 401(k) plan.

Most self-employed retirement plans allow for contributions to be made as late as October 15th of the following year. This benefit is really cool as it allows you to calculate various levels of savings based on various contribution amounts. The 2018 maximum contribution allowable for these plans can be as high as $61,000 if catch-up contributions are permitted for taxpayers age 50 and older.

-

- Increase Tax-favored Income. Converting taxable interest to tax-exempt interest will serve to reduce adjusted gross income and modified adjusted gross income. For example, moving money from CDs or money market accounts will not create any taxable income. Alternatively, selling corporate bonds may produce a taxable gain and reduce or offset the benefits.

- Reduce Business or Rental Real Estate Income. Make full use of depreciation including bonus depreciation and Section §179 expensing allowances for property and equipment placed in service before the end of the year. You have more control in attaining the desired profit or loss level if properly analyzed. The 2017 Tax Cut and Jobs Act allows for more favorable treatment of certain building improvements in 2018 and beyond. For example, essentially any improvement to nonresidential roofs, including a full replacement for existing buildings, may be expensed in the year of purchase by any taxpayer eligible to deduct under Section §179. These type expenditures have historically been subject to much longer depreciation recovery periods.

Capital Gains and Losses

Looking at your investment portfolio can reveal several different tax-saving opportunities. Review your year-to-date sales of stocks, bonds and other investments. This allows you to determine the net amount of capital gains or losses you have realized to date. Also, review the unsold investments in your portfolio to determine whether these investments have an unrealized gains or losses. (Unrealized means you still own the investment while realized means you’ve sold the investment).

Most taxpayers are able to obtain the tax basis of their investments. In most instances, basis refers to the price that you paid to acquire the investment. Some investments allow you to reinvest your dividends and/or capital gains to purchase additional shares. These additional shares add to the cost basis of the original purchase.

If your capital gains are larger than your losses, you can begin looking for tax-loss selling candidates. This strategy called “loss harvesting” converts the unrealized losses to realized losses. Tax loss harvesting and portfolio rebalancing are a natural fit. If you’re more of a buy and hold mutual fund investor, your capital gains may be in the form of mutual fund distributions. These distributions are typically paid out towards the end of the tax year and sometimes can be quite substantial. Implementing the “loss harvesting” strategy after these additional gains are included provides for more accurate tax planning. The tax code allows you to apply to up to $3,000 of net capital losses to reduce ordinary income items such as interest, dividends and wages. Any remaining unused capital losses can be carried forward into future years indefinitely.

Please note that if you sell an investment with a loss and then buy it right back, the IRS disallows the deduction. The “wash sale” rule says you have to wait at least 30 days before buying back the same security in order to be able to claim the original loss as a deduction. However, you can buy a similar security to immediately replace the one you sold—perhaps a stock in the same sector. This strategy allows you to maintain your general market position while utilizing a tax break.

Zero Percent Tax on Long-Term Capital Gains

If you are in the 10% or 12% tax bracket, the tax rate for long-term capital gains is zero percent! In order to qualify for this tax break, your 2018 taxable income cannot exceed $38,700 for singles and $77,400 for married joint filers.

Please note that the 0% tax rate only applies until your taxable income exceeds the current 12% tax bracket. For example, let us assume that a married couple with wages of $70,000, long-term capital gains of $40,000 and deductions of $14,700 leaving them with $95,300 of taxable income. The first $22,100 of long-term capital gain is tax-free, but once their taxable income passes the $77,400 limit, the remaining long-term capital gain of $17,900 is taxed at 15%.

If you are eligible for the 0% capital gains tax rate, here is a cool maneuver. It might be appropriate to sell some appreciated stocks to take advantage of the zero percent capital gains rates. Sell just enough so your gain pushes your income to the top of the 12% tax bracket, then buy new shares in the same company. The newly purchased shares will have a higher cost basis than the shares you sold. If you should eventually sell these shares, it will be with a new higher tax basis. This allows you to take advantage of the 0% tax rate now. Please also note that you do not have to wait 30 days before you can buy the stock back when there is a taxable gain. This technique is referred to as “gains-harvesting.” The 30 days period only applies to securities sold at a loss.

Consider this strategy. If you’re ineligible for the 0% capital gains tax rate, but you have adult children (not subject to the Kiddie tax rules) in the 0% bracket, consider gifting appreciated stock to them. Your adult children will pay a lot less in capital gains tax than if you sold the stock yourself and gifted the cash to them. This is especially true if you are subject to both the Medicare surtax on net investment income, and you’re in the 37% tax bracket. In this scenario, you are paying 23.8% on your long-term capital gains. Modest amounts of low basis stocks can still be gifted and sold by younger children while avoiding the new Kiddie tax rules in effect.

But be careful—you can’t “go back in time” if you subsequently discover you would have fared better had you identified different shares before you made a particular sale. If you don’t specify which shares you are selling at the time of the sale, the tax law treats the shares you acquired first as the first ones sold. In other words, it uses a FIFO (First-In, First-Out) method. This may not produce the optimal result that you had wished for.

Hidden Gem. When a parent’s income is too high to claim education tax credits, (the American Opportunity and Lifetime Learning) shifting income to the kid’s return can generate tax savings. In this tax-planning strategy, the parent is eligible to claim the child as a dependent but chooses not to on the parent’s tax return. Although, the parent is giving up the child as a dependent on their tax return, the child “can’t” claim a personal exemption for themselves on their own tax return. By waiving the dependency deduction, the parent also gives up the right to claim the college tax credit on their return. Keep in mind the parent wouldn’t be eligible to take the tax credit on their tax return so no loss there.

The kid is now able to claim the education credit on their own tax return up to $2,500 depending on which education credit they’re eligible for. This is even true if the parent pays for the college tuition and qualified expenses. Ideally you would shift enough long-term capital gain income from the parent to the child to be offset by the $2,500 education tax credit. Caution: Take into effect the changes to the Kiddie Tax rules when calculating the optimal amount.

Shifting income from a parent to a minor child can help save taxes. Once again, be sure you take into consideration the new Kiddie tax rules otherwise you may end up not achieving what you set out to do.

Step-Up-In-Basis Rules

Another very important but often overlooked item is a step-up-in-basis, which occurs when a taxpayer inherits certain assets. The new cost basis is the fair market value as of the date of death, which is often much greater than the original basis that the decedent had in this investment. However, the step-up-in-basis rule does not apply to certain investments, such as IRAs and other tax-deferred accounts.

Remember that if someone gifts you an appreciated asset while they are alive, then the recipient’s basis is the same as the basis of the giver.

Taxes on Social Security Income

Social Security income may be taxable, depending on the amount of other income a taxpayer receives. If a taxpayer only receives Social Security income, the benefits are generally not taxable, and it is possible that the taxpayer may not even need to file a federal income tax return.

If a taxpayer receives other income in addition to Social Security income, and one-half of the Social Security income plus the other income exceeds a base amount, then up to 85% of the Social Security income may be taxable. The base amount is $25,000 for a single filer and $32,000 for married taxpayers filing a joint return.

A complicated formula is necessary to determine the amount of Social Security income that is subject to income tax. IRS publication 915 contains a worksheet that is helpful in making this determination.

Social Security income is included in the calculation of MAGI for purposes of calculating the Medicare contribution tax, as discussed earlier. Therefore, taxpayers having significant net-investment income will have a reason to delay receiving Social Security benefits.

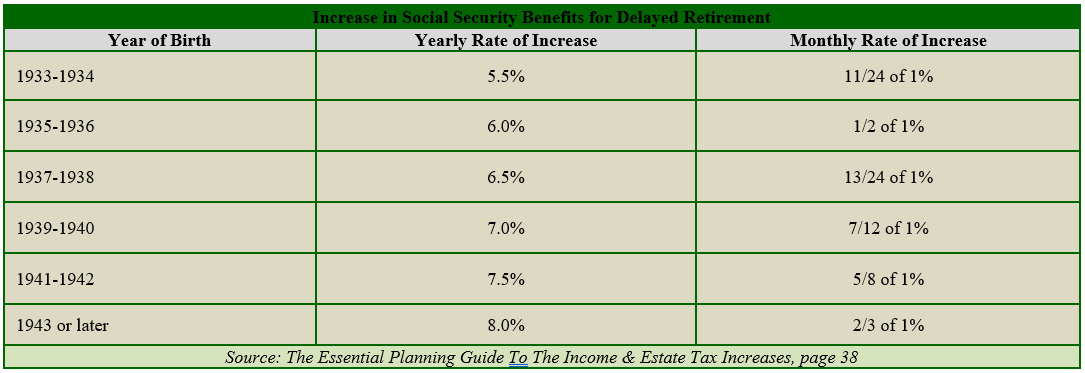

Assuming a reasonable or long life expectancy, it is generally beneficial for an individual who is eligible to receive Social Security on or after age 62 to delay payments until full retirement age. Assuming a full retirement age of 66, an individual who elects to receive Social Security benefits at age 62 will see benefits reduced by 25%. However, if the same individual delays receiving Social Security benefits until after full retirement age, a delayed retirement credit may be available. The chart below shows the percentage increases when an individual delays receipt of retirement benefits.

An interesting wrinkle in long-term planning related to the taxation of Social Security is the synergy of developing a good long-term Social Security maximization plan and a good long-term Roth IRA conversion plan. We often enjoy tremendous benefits using the following combination strategy under the right circumstances.

One effective strategy is holding off on Social Security and making Roth IRA conversions in the years after you retire and you don’t have wages, but before age 70 when you will have Required Minimum Distributions (RMD) and full Social Security. Make those Roth IRA conversions while your marginal income tax bracket is at an all-time low. Please note a Roth IRA conversion increases income which could increase Social Security taxes.

On November 2, 2015, President Obama signed the Bipartisan Budget Act (BBA) of 2015 into law. This law eliminated two of the most effective methods available for maximizing Social Security benefits: Apply and Suspend and filing a Restricted Application for benefits. For an excellent and concise explanation of these new rules please see my The Little Black Book of Social Security Secrets at https://paytaxeslater.com/ss. We do “run the numbers” and provide personalized solutions for both Social Security maximization and Roth IRA conversions for our assets under management clients.

Estate and Gift Tax Opportunities

The game of estate planning for most clients has changed from trying to reduce gift or estate tax to trying to reduce income taxes. For 2018, each taxpayer can pass $11,180,000 (minus past taxable gifts that he/she has made) to children or other beneficiaries without having to pay gift or estate taxes. The exemption increases to $11,400,000 in 2019. If you are married, you will be able to pass $22,800,000 without any federal gift or estate taxes. There is a 35% estate tax on gifts or estates of deceased persons exceeding the limits. This is the exemption amount for federal estate tax, not for PA inheritance tax, which is a flat 4.5% to lineal heirs (children and grandchildren).

Many people believe that with the estate tax exemption set at over $11,000,000 per person, they don’t need to worry about shrewd, tax-wise ways to give wealth. However, these people might want to rethink their strategy. Congress can change the law (and has changed the law in the past), and your wealth could grow faster than expected, thereby subjecting you to estate tax. Nevertheless, before you gift something away, you need to consider the income tax effects of making certain gifts. Giving away the wrong asset can cost your family some unnecessary taxes. However, if you have an estate that is worth less than $3,000,000, I would recommend focusing on long-term planning to reduce income taxes, not estate taxes. Planning appropriately for your IRA, Roth IRA, Roth IRA conversions and your retirement plan should be your biggest concern.

Many people believe that with the estate tax exemption set at over $11,000,000 per person, they don’t need to worry about shrewd, tax-wise ways to give wealth. However, these people might want to rethink their strategy. Congress can change the law (and has changed the law in the past), and your wealth could grow faster than expected, thereby subjecting you to estate tax. Nevertheless, before you gift something away, you need to consider the income tax effects of making certain gifts. Giving away the wrong asset can cost your family some unnecessary taxes. However, if you have an estate that is worth less than $3,000,000, I would recommend focusing on long-term planning to reduce income taxes, not estate taxes. Planning appropriately for your IRA, Roth IRA, Roth IRA conversions and your retirement plan should be your biggest concern.

In 2018, you and your spouse can each give $15,000 per calendar year ($30,000 for couples) to as many individuals as you’d like without reducing your lifetime gift tax exemptions. Depending on your circumstances, it may be smart to make a gift before the end of this year. Gifts to medical or educational providers are not included in the $15,000 limit. In fact, there is no limit on qualified gifts as long as the check is made directly to a school or medical facility.

If you are going to make a gift, it is important to determine which asset is the best one to gift. It is usually best to gift high-basis assets or cash, especially if the taxpayer is in poor health. In most cases, it is best not to give low-basis assets because the basis of gifted assets is the same for the recipient as it is for the donor, and the gifted assets will not usually receive a step-up-in-basis when a taxpayer passes.

Before making sizable gifts to children or other family members, keep in mind that in some cases, these gifts may unfortunately backfire. For example, a gift might make a student ineligible for college financial aid, or the earnings from the gift might trigger tax on a senior’s Social Security benefits.

Congress has created a number of tax breaks over the last few years to help pay for education. One of the most popular types of savings plans is the 529 plan. Withdrawals (including earnings) used for qualified education expenses (tuition, books and computers) are income-tax free.

The amount you can contribute to a Section 529 plan on behalf of a beneficiary qualifies for the annual gift-tax exclusion. However, the tax law allows you to give the equivalent of five years’ worth of contributions up front with no gift-tax consequences. The gift is treated as if it were spread out over the 5-year period. For instance, you and your spouse might together contribute the maximum of $150,000 (5 x $30,000) on behalf of a grandchild this year without paying any gift tax.

Miscellaneous Year-End Tax Reduction Strategies

Most taxpayers cannot control the timing of received income, but many of us can determine when to pay or not pay deductible expenses. Prepare tax projections for 2018 and possibly 2019 to determine which tax bracket you are in and where you can get the most bang for your buck. The projections may also help minimize AMT and reduce the Medicare surtaxes. Let’s say for example, your deductions and exemptions are greater than your income, and you will have a negative taxable income, with a tax liability of zero. This is often the case with seniors who receive tax-free Social Security income. In this case, it would be a good strategy to increase your income from negative taxable income to zero taxable income, because the tax on zero taxable income is still zero! One of the best ways to do this is to do a partial Roth IRA conversion up to the amount that brings your negative taxable income up to zero. Depending on your tax bracket, you may wish to convert even more, especially if you expect to be in a higher income tax bracket in the future. If a Roth conversion is not appropriate or desirable, then taking additional retirement account distributions in one year while lowering the amount in the following year may save tax dollars. This strategy is comparable to bunching itemized deductions while using income instead of expenses.

Paying taxes is bad enough. Paying a penalty is even worse. If you face an estimated tax shortfall for 2018, and you haven’t received your 2018 Required Minimum Distribution payment consider having the extra tax withheld on the IRA distribution. Withheld taxes are treated as if you paid them evenly to the IRS throughout the year. This can make up for any previous underpayments, which could save you penalties.

If you turned age 70 ½ during 2018, you still have until April 1, 2019 to withdrawal your first RMD. This is a one-time opportunity in case you forgot. Remember—if you do not take out your RMD by this date, you will be faced with a 50% penalty on the failed distribution amount. Before holding off until April 1, 2019 to take your first RMD, review the tax implications especially if you’re likely to be subject to the Medicare surtax on net investment income. (NOTE: If your first RMD is due by April 1, 2019, you will be responsible for taking out two RMDs in 2019. This will often put you in a higher tax bracket in 2019. Therefore, a two-year tax projection is usually recommended before deciding whether it’s more tax advantageous to take your first RMD by the end of the current tax year or choosing to defer the first payment into the following tax year and paying taxes on two RMD payments in year two.

Harvesting Ordinary Income. Harvesting ordinary income is another part of an overall successful year-end plan. Many older taxpayers incur extraordinary high medical expenses. Without proper planning, thousands of dollars of medical expenses can be incurred with no tax benefit. Harvesting ordinary income should at least equal itemized deductions plus exemptions; and the targeted tax liability at least equals tax credits available. Furthermore, harvesting ordinary income may be considered in order to “fill up” your marginal tax bracket.

Making Trust Distributions. Net investment income tax also applies to trusts and estates. With compressed tax brackets for trusts compared to individual tax brackets, making permitted discretionary distributions to beneficiaries can reduce overall taxes. By making the proper election, trusts can distribute current year income up to 65 days into the following year and still have the income taxed to the beneficiary in the current tax year.

Pennsylvania 529 Plan Contribution Deduction. Don’t miss out on the state tax deduction for contributions to a Section 529 College Saving Program. A taxpayer can reduce their PA taxable income up to $15,000 per plan beneficiary (kids, grandkids, nieces, nephews, etc.). Married couples can deduct up to $30,000 per beneficiary per year, provided each spouse has taxable income of at least $15,000. If your child is currently in college and you are writing checks to the college for tuition or qualified expenses, you should open the 529 plan immediately. You can deposit the college expense money into the account and immediately write the check to the college. You have just generated an immediate 3.07% rate of return on the deposit. Now that’s a winner.

529 Plan changes. The 2017 TCJA provides that distributions up to $10,000 used for tuition at an elementary or secondary public, private or religious school,K-12 are permitted. Prior law limited 529 money to be used to pay college and/or graduate school costs.

Kiddie Tax Planning. Considering hiring your child as an employee. A child can use their standard deduction to shelter up to $12,000 of wages from federal income tax compared to $6,350 in 2017. Also, the child becomes eligible to contribute up to $5,500 to a Roth IRA. The wage income may enable the child to escape the kiddie tax rules that would otherwise be imposed on unearned income.

Utilize Your Home Office. It may be the right year to switch back to deducting the actual cost of home office expenses as opposed to using the simplified method. If you are one of the many who will be using the standard deduction in 2018, enjoying some tax benefits of deducting a portion of your real estate and mortgage interest as a home office deduction can help ease the pain.

Employee Business Expenses. With the elimination of deductions formerly reported on Form 2106 Employee Business Expense, encourage your employer for reimbursement of the substantiated expenses that are no longer tax-deductible.

Charitable Giving

Under the current tax system, a focus on controlling adjusted gross income can provide tax savings. The Path Act of 2015 made permanent the popular Qualified Charitable Distribution (QCD) rules for making charitable contributions from an IRA. Taxpayers age 70 ½ and older can transfer up to $100,000 directly from their IRA over to a charity, satisfying all or part of the RMD with the IRA-to-charity maneuver. Please read the June 2016 Lange Report at https://paytaxeslater.com/lange-report/lange-report-june-2016/ for a great summary of how seniors can get more out of their charitable giving.

Under the current tax system, a focus on controlling adjusted gross income can provide tax savings. The Path Act of 2015 made permanent the popular Qualified Charitable Distribution (QCD) rules for making charitable contributions from an IRA. Taxpayers age 70 ½ and older can transfer up to $100,000 directly from their IRA over to a charity, satisfying all or part of the RMD with the IRA-to-charity maneuver. Please read the June 2016 Lange Report at https://paytaxeslater.com/lange-report/lange-report-june-2016/ for a great summary of how seniors can get more out of their charitable giving.

This is a great time of the year to clean out your basement and garage. However, please remember that you can only write off these non-cash charitable donations to a charitable organization if you itemize your deductions. Please do yourself a favor and follow the substantiation rules to tilt the scale in your direction if the deduction is questioned by the IRS. Determining the value of non-cash donations can sometimes be challenging. You can find estimated values for your donated clothing at http://turbotax.intuit.com/personal-taxes/itsdeductible/. It can never hurt to have pictures of the donated items (cell phones cameras make this much easier). The more detailed the receipt, the better. Please send cash donations to your favorite charity no later than December 31, 2018 and be sure to hold on to your cancelled check or credit card receipt as proof of your donation. If you contribute $250 or more, you also need an acknowledgement from the charity. Many taxpayers kindly help out various charities making non-cash donations.

Tax tip for coaches who still itemize their charity deductions: Many taxpayers have children who participate in youth, intermediate or even high school level sports. If dad or mom volunteer their time as coaches, assistant coaches, timekeepers etc. they can be eligible for an income tax deduction for various out-of-pocket expenses incurred. For example, miles driven on their cars while performing their role as coach are deductible charity miles. Many teams travel out of town to compete. You are entitled to deduct certain travel expenses as a charitable deduction. See the IRS website Newsroom for “Tips for Taxpayers Who Travel for Charity Work” for a list of qualifying deductions.

My favorite substantial charitable gift is leaving a portion of your IRA or retirement plan to a charity of your choice after you and your spouse die.

If you want to give money to a charity and get the deduction this year, but don’t know which charity you want to benefit, you should consider donor directed funds that could be set up by a group like The Pittsburgh Foundation.

As mentioned earlier, if you plan to make a significant gift to charity this year, consider gifting appreciated stocks or other investments that you have owned for more than one year. Doing so boosts the savings on your tax returns. Your charitable contribution deduction is the fair market value of the securities on the date of the gift, not the amount you paid for the asset, and therefore, you never have to pay taxes on the profit!

Do not donate stocks that have lost value. If you do, you can’t claim a loss. In this case, it is best to sell the stock with the loss first and then donate the proceeds, allowing you to take both the charitable contribution deduction and the capital loss.

Inherited IRAs

Be careful if you inherit a retirement account. In many cases, a decedent’s largest asset is his or her retirement account. When a beneficiary receives this distribution, it is often a very large sum of money, and there is no step-up-in-basis on retirement accounts. If you inherit a retirement account, such as an IRA or other qualified plan, the money is usually taxable upon receipt. In addition to this immediate taxation, the extra money could push you up into a higher tax bracket, causing you to pay more taxes than you might have if this taxable income was spread over several years.

The solution to this problem is to establish an Inherited IRA, allowing you to spread out the distributions over your lifetime which should reduce and defer your income taxes significantly. Sounds easy, right? Unfortunately, the tax laws regarding the inheritance of retirement accounts are very complicated. Be sure to take the necessary steps in order to avoid any unnecessary income taxes.

Helpful Tip. Inherited IRAs for non-spouse beneficiaries can never be converted to a Roth IRA. Inherited employer plan assets (401k), 403(b) etc. can be directly transferred to a properly titled, inherited Roth IRA. Income tax will be due on the conversion and paid by the beneficiary. Required distributions will also occur. If the child beneficiary is in a lower tax bracket at the time of inheritance what a wonderful way to get a Roth IRA started at a lower tax cost while enjoying future tax-free growth. Step to take. You may want to help direct mom and/or dad after they retire to keep some of their retirement plan dollars in a qualified plan rather than rolling everything into a traditional IRA.

Identity Theft Affidavit: Consider filing IRS Form 14039 (available on the IRS website) before the 2016 tax filing season arrives. Identity theft has been steadily on the rise. The IRS will provide you a 6-digit PIN number to use when filing your income tax return. The PIN will help the IRS verify a taxpayer’s identity and accept their electronic or paper tax return. The PIN will prevent someone else from filing a tax return with your SSN as the primary or secondary taxpayer (spouse).

IRS Scams: Threatening emails and phone calls purporting to be from the IRS have been proliferating—don’t get caught in a scam. Please read the article in the October 2016 Lange Report for helpful facts at https://paytaxeslater.com/lange-report/lange-report-october-2016/.

Instructions for prepaying your 2019 City of Pittsburgh and Allegheny County Real Estate Taxes.

For the Allegheny County Taxes the mailing address is:

John K Weinstein, County Treasurer

Room 108 Courthouse Building

436 Grant Street

Pittsburgh, PA 15219

Attention Mary Lee

You will include a note indicating that you are prepaying your 2019 Real Estate Taxes. The amount you will pay will be the same as you paid in 2018. If you know your lot and block number or your account number include it on the memo line of the check. If you don’t know that information they will be able to obtain your name and address on the check that you’re sending and apply the payment properly.

For the City & School Real Estate Taxes the mailing address is:

Real Estate Tax Division

414 Grant Street

Pittsburgh, PA 15219

Attention Collen Salmon

Follow the same instruction as above.

Final Thoughts: When it comes to tax planning and paying income taxes it’s usually not what you know, but rather what you don’t know that can leave you with unhappy tax results. We are here to help close that knowledge gap. We look forward to seeing you soon.

About Glenn Venturino, CPA: Glenn has been an integral part of the Lange Accounting Group, LLC for over 30 years. As our longest standing Lange team member, Glenn manages the tax department and oversees many of the day-to-day operational functions such as payroll, employee benefits, financial reporting and billing. As a CPA, Glenn has built a substantial accounting practice having working relationships with hundreds of individual clients and various small businesses.

About Jim Lange, CPA/Attorney: James Lange is President of Lange Financial Group, LLC and has 30+ years of experience working with retirees and those about to retire. Jim can be reached at (412) 521-2732.

The views expressed are not necessarily the opinion of Lange Financial Group, LLC and should not be construed, directly or indirectly, as an offer to buy or sell any securities mentioned herein. This article is for informational purposes only. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice as individual situations will vary. For specific advice about your situation, please consult with a financial professional.

Some Content Provided by MDP, Inc. Copyright MDP, Inc.

|

Help us grow in 2019!

Help us grow in 2019!