Bill Bengen’s New 30-Year Safe Withdrawal Rate: A 17.5% Raise for Retirees

by James Lange, CPA/Attorney

Reprinted with permission of Forbes.com where Jim is a paid contributor.

Bill Bengen’s research on retirement withdrawals has shaped financial planning for decades. He is widely recognized as the originator of the “4% rule,” a guideline that has been referenced in countless academic papers, financial planning articles, and media discussions about how retirees can safely draw income from their portfolios.

In his latest research, Bill unveils an updated safe withdrawal rate for a traditional 30-year retirement horizon—raising it from 4.0% to 4.7%. This increase effectively represents a 17.5% raise for retirees who follow the framework. The updated guidance is explained in detail in his book A Richer Retirement: Supercharging the 4% Rule to Spend More and Enjoy More.

This article draws heavily on Bill Bengen’s groundbreaking research and recent updates. Bill was kind enough to review this article, and his insights are incorporated throughout.

The Math Behind the Change from 4.0% to 4.7% — A 17.5% Raise

The increase from 4.0% to 4.7% stems primarily from updated assumptions. In the past, Bill based his calculations on a simple 50/50 portfolio of U.S. stocks and bonds. His new model assumes a well-diversified portfolio consisting of multiple asset classes.

For retirees, the impact can be meaningful. In the first year of retirement, a retiree with $1 million in savings could withdraw $47,000 instead of $40,000. That $7,000 increase represents a 17.5% raise in spending power.

Reminder of How Bill’s Safe Withdrawal Rate Works

The method begins by withdrawing 4.7% from your retirement portfolio during the first year. In each following year, you increase that initial withdrawal amount by the annual inflation rate—regardless of how the market performs.

For example, if you withdraw $47,000 in year one and the portfolio declines to $850,000 by the end of that year while inflation runs at 3%, your year-two withdrawal would still be based on the first-year withdrawal amount. In this case, you would increase the $47,000 by 3%, resulting in a withdrawal of $48,410 in year two.

Why Investment Horizons Matter

Few retirees have a perfectly defined 30-year investment horizon. Some individuals will need retirement income for only a few years, while others may require income for forty or even fifty years.

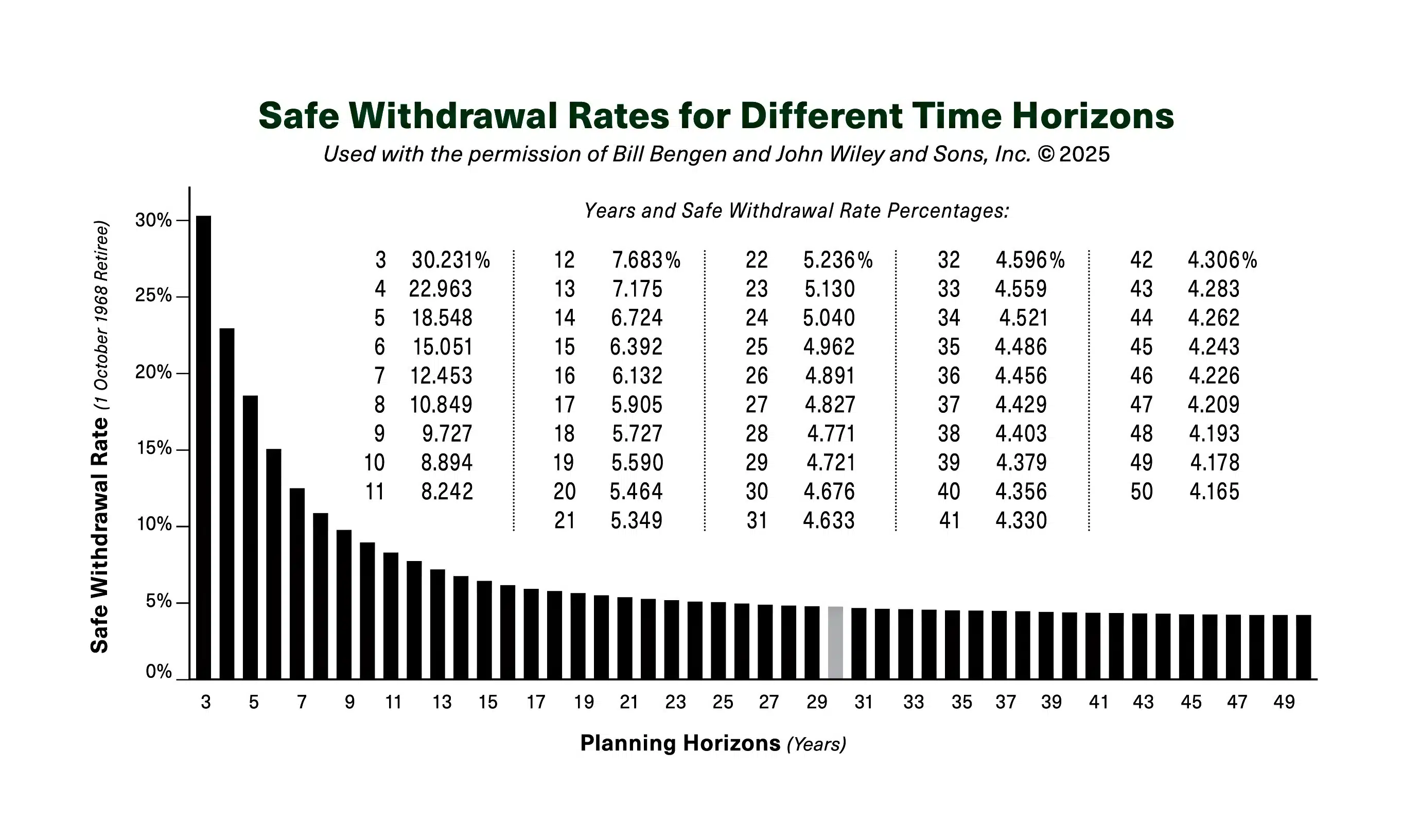

Bill’s updated research includes a chart showing safe withdrawal rates for investment horizons ranging from 3 to 50 years. The chart, reproduced from page 81 of his book, provides a practical roadmap for retirees who want to match their withdrawal strategy to their own realistic planning horizon rather than relying on a one-size-fits-all rule.

For example, someone with a ten-year investment horizon could safely withdraw about 8.894%, while someone planning for twenty years could withdraw about 5.464%.

What the Chart Reveals and Why it Could Be Life Changing

What the Chart Reveals and Why it Could Be Life Changing

The chart illustrates withdrawal percentages over a 50-year timeline using the experience of retirees who began retirement on October 1, 1968—the worst retirement start date in recorded U.S. history.

Those retirees experienced both a severe bear market and the high inflation of the 1970s. Even under those historically difficult conditions, the updated withdrawal rates held up. This makes the projections conservative, meaning that most retirees are likely to experience outcomes that are even better.

The Practical Impact for Retirees

Understanding safe withdrawal rates allows retirees to estimate how much they can confidently spend without worrying about running out of money.

Beyond the math, the lifestyle implications can be significant. Safely spending more may allow retirees to travel more frequently, pursue hobbies, or enjoy meaningful experiences with family.

My father-in-law, who is 101 years old, sponsors an annual family vacation for all of his children, spouses, grandchildren, and now great-grandchildren. What a legacy! Experiences like these often provide far greater long-term satisfaction than material purchases.

Alternatively, some retirees may choose to make financial gifts to their children when they need it most rather than leaving everything as an inheritance later. Even if you ultimately decide not to increase your spending, the updated research may at least reduce the fear of outliving your money.

If Leaving a Legacy Is a Goal

If you want to preserve assets for heirs, you can adjust your withdrawal rate accordingly. For example, one projection assumes a starting portfolio of $1,000,000 with a 30-year horizon. By reducing the withdrawal rate from 4.67% to about 4.21%, the model suggests you could leave a legacy of at least $500,000 in today’s dollars.

Caveats and Conclusion

No financial model is immune to risk. A historically unprecedented sequence of poor market returns could disrupt even the most carefully constructed framework. Bill himself acknowledges that other withdrawal methods also exist.

However, his framework remains one of the most widely recognized and extensively studied approaches to retirement spending. After more than thirty years of analysis and testing, it continues to provide a practical foundation for retirement planning.

Whether your planning horizon is 3 years, 30 years, or 50 years, Bill’s updated research offers retirees a valuable roadmap for spending confidently while minimizing the risk of running out of money.

Additional Planning Considerations

While Bill’s research focuses on withdrawal rates, a comprehensive retirement plan should also consider tax planning and estate strategies. The suggestions below are not Bill’s, but mine, and there are many exceptions.

- Optimize Social Security planning so that the spouse with the stronger earnings record waits until age 70 to collect.

- Consider the equity in your home by evaluating options such as a HELOC or reverse mortgage.

- Evaluate the potential role of immediate annuities for retirees with long life expectancies.

- Consider a series of Roth IRA conversions.

- Spend after-tax dollars first, then traditional IRAs, and Roth IRAs last.

- Prepare estate planning documents utilizing Lange’s Cascading Beneficiary Plan℠.

When it comes to determining how much money you can safely withdraw from your retirement portfolio, Bill Bengen’s research remains one of the most influential frameworks available. Applying his insights can help retirees pursue both financial security and a fuller, more enjoyable retirement.

About James Lange, CPA/Attorney

Jim is the author of 10 best-selling financial books and has been quoted 37 times in The Wall Street Journal. He has published 21 articles for Forbes.com.