*Please note this blog post is a repost with permission from Forbes.com

On May 23, 2019, the House of Representatives overwhelmingly passed the SECURE Act (Setting Every Community Up for Retirement Enhancement). A more appropriate name for the bill would be the Extreme Death-Tax for IRA and Retirement Plan Owners Act because it gives the IRS carte blanche to confiscate up to one-third of your IRA and retirement plans. In other words, it’s a money grab.

The SECURE Act is wrapped with all kinds of goodies that are unfortunately of limited benefit to most established IRA and retirement plan owners. But if you have an IRA or a retirement plan that you were hoping you could leave to your children in a tax-efficient manner after you are gone, you need to be concerned about one provision in the fine print that could cost them dearly. Non-spouse beneficiaries of IRAs and retirement plans are required to eventually withdraw the money from its tax-sheltered status, but the current law allows them to minimize the amount of their Required Minimum Distributions by “stretching” them over their own lifetimes. This is called a “Stretch IRA”. Distributions from a Traditional Inherited IRA are taxable, so the longer your beneficiaries can postpone or defer them (and hence the tax), the better off they will be. The bad news is that the government wants their tax money, and they want it sooner than later. The ticking time bomb buried in the SECURE Act is a small provision that changes the rules that currently allow your beneficiaries to take distributions from Traditional IRAs that they have inherited and pay the tax over their lifetimes, virtually cementing “the death of the Stretch IRA.” (The provisions of the SECURE Act also apply to Inherited Roth IRAs, but the distributions from a Roth IRA are not taxable.)

If there is any good news about the SECURE Act, it’s that it does not require your beneficiary to liquidate and pay tax on your entire Traditional IRA immediately after your death. For many people, that would be a costly nightmare because they would likely be bumped into a much higher tax bracket. Under the provisions of the SECURE Act, if you leave a Traditional IRA or retirement plan to a beneficiary other than your spouse, they can defer withdrawals (and taxes) for up to 10 years. (There are some exceptions for minors and children with disabilities etc.) If you leave a Roth IRA to your child, they will still have to withdraw the entire account within 10 years of your death, but again, those distributions will not be taxable. But any way you look at it, the provisions of the SECURE Act are a huge change from the old rules that allow a non-spouse heir to “stretch” the Required Minimum Distributions from a Traditional Inherited IRA over their lifetime and defer the income tax due.

That’s not the end of the bad news. Once your beneficiary withdraws all the money from your retirement account, it will no longer have the tax protection that it currently enjoys. In other words, even if your children inherited a Roth IRA from you and the distributions themselves weren’t taxable, the earnings on the money that they were required to withdraw are another story. Even if they wisely reinvest all the money they withdrew from their Inherited Traditional or Roth IRA into a brokerage account, they’re still going to have to start paying income taxes on the dividends, interest and realized capital gains that the money earns.

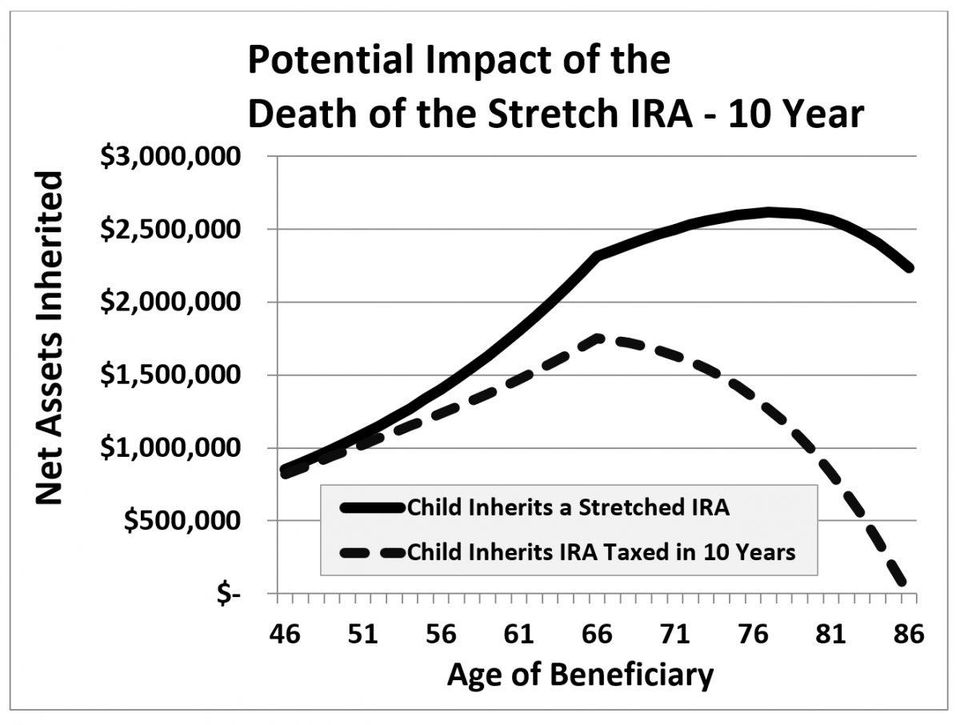

I know there are readers out there who are thinking “it can’t be all that bad”. Yes, it is that bad. Here is a graph that demonstrates the difference between you leaving a $1 million IRA to your child under the existing law, and under the SECURE Act:

Child Inherits Stretched IRA Under Existing Law versus Child Inherits 10 Year IRA Under SECURE Act – James Lange

This graph shows the outcome if a $1 million Traditional IRA is inherited by a 45-year old child, and the Minimum Distributions that he is required to take are invested in a brokerage account that pays a 7 percent rate of return. Other assumptions are listed below*. The only difference between these two scenarios is when your child pays taxes! The solid line represents a child who can defer (or “stretch”) the taxes over his lifetime under the existing rules. At roughly age 86, that beneficiary who was subject to the existing law in place still has $2,000,000+. The dashed line represents the same child if he is required to take withdrawals under the provisions of the SECURE Act. At age 86, that same beneficiary has $0. Nothing. Nada. The SECURE Act can mean the difference between your child being financially secure versus being broke, yet Congress is trying to gloss over this provision buried in the fine print. I don’t think so!

The House of Representatives passed the SECURE Act by an overwhelming majority, so the probability that the Senate will pass a version of this legislation is quite good. In 2017, the Senate Finance Committee recommended the Death of the Stretch IRA by proposing the Retirement Enhancement and Savings Act (RESA). In true government fashion, RESA was unbelievably complicated. It allowed your non-spouse beneficiaries to exclude $450,000 of your IRA and stretch that portion over their lifetime – but anything over that amount had to be withdrawn within five years and the taxes paid. And if you had more than one non-spouse beneficiary, the amount that they’d be able to exclude from the accelerated tax would have depended on what percentage of your Traditional IRA they inherited. Imagine trying to plan your estate distribution around those rules!

The Senate is now floating an updated RESA 2019 that seems to say that it will change the original exclusion amount to $400,000. It will be a good change if it is passed. That is because instead of each IRA owner getting a $400,000 exclusion, the new version includes language to allow a $400,000 exclusion per beneficiary. When I first read that provision I thought I had either read it wrong or that it was a typo. That little detail would be extremely valuable (and make estate planning for IRAs and retirement plans far more favorable), especially for families with more than one child. But even in the Senate version, anything over and above that exclusion amount will have to be distributed (and the taxes paid) within five years of your death (instead of ten years like the House version).

Unfortunately, our “peeps” think the House version of the bill (which has a 10-year deferral period, but no exclusion) will be what eventually becomes law. This is particularly troubling because the Senate version would allow room for far more creative planning opportunities (and tax savings, because of the $400,000 per beneficiary exclusion). As of the time of this post, Senator Cruz is attempting to hold up the bill, but his reasons have nothing to do with the fine print that affects Inherited IRAs. The original version of the Act contained provisions about college tuition (Section 529) plans, but those provisions were stripped in the version the House voted on and Senator Cruz wants them restored. Unfortunately, no one is arguing about the biggest issue with the SECURE Act, which is the massive acceleration of distributions and taxes on your IRA after your death. And unless someone in Congress objects to the provision in the SECURE Act about Inherited IRAs, your non-spouse beneficiaries will find out the hard way that their elected officials have quietly arranged to pick your pockets upon your death.

I have been a popular guest on financial talk radio lately. Many of the hosts want to blame one political party or the other. I blame all of Congress. This is one of the few truly bipartisan bills that has potential devasting consequences, at least for my clients and readers, and it is highly likely to pass both sides of Congress. I wonder how many of our legislators in the House actually read this bill or understood what is was they voted for. Did they realize they are effectively—by accelerating income-tax collection on inherited IRAs and other retirement plans—imposing massive taxes on the families of IRA and retirement plans owners – even those with far less than a million dollars? Or perhaps they did understand it and hoped that the American public wouldn’t.

If you can’t tell by my tone, I am upset. I am also motivated to examine every strategy that we can use to legally avoid, or at least mitigate, the looming hammer of taxation on your Traditional IRAs and retirement plans. I’m going to address these strategies in a series of posts, so please read them to see how this proposal could affect someone in your specific situation. Even though the Senate version has a five-year tax acceleration instead of a ten-year, the Senate version could be better for most readers because of the value of the exclusion – especially if you have multiple beneficiaries.

Please check for follow-up posts on this subject. I will show you some strategies to protect your family from the Death of the Stretch IRA and keep more of your hard-earned money in your hands.

James Lange

- Assumptions used for Graph

- $1 Million Traditional IRA inherited by 45-Year Old Married Beneficiary

- 7% rate of return on all assets

- Beneficiary’s salary $100,000

- Beneficiary’s annual expenses $90,000

- Beneficiary’s Social Security Income at age 67 $40,000

My wife recently told me that she didn’t think that there was anything that could keep me from blogging about my upcoming book, Retire Secure! While she was joking, she was also right, I thought. But then,

My wife recently told me that she didn’t think that there was anything that could keep me from blogging about my upcoming book, Retire Secure! While she was joking, she was also right, I thought. But then,