Spend the Right Money First When You Retire

(Including a New Wrinkle in Our Bedrock Principle)

by James Lange, CPA/Attorney

Reprinted with permission of Forbes.com where Jim is a paid contributor.

For more than twenty years, I have advocated “Pay Taxes later, except for the Roth.” This applied in the accumulation stage when you are accumulating money for retirement, the distribution stage when you are deciding which assets to spend first, and even in the estate planning stage. I always said there were some exceptions to this bedrock foundational principal, but this was a great starting point for general advice.

Since the SECURE Act became effective on January 1, 2020, the exception to this general rule became much bigger for many IRA and retirement plan owners.

What follows comes from our newest book, Retire Secure for Professors, which has great information for all IRA owners. Non-professors could skip the chapters on TIAA and still get a lot of value from the book. Please see the end of this article to learn how you can request a copy of the book for you and/or any friends or colleagues who you think might find it valuable.

Following is an excerpt from Retire Secure for Professors:

The next big question is: In what order should you spend the money you have saved for retirement? Subject to exception, you should spend your after-tax dollars before your retirement plan or IRA dollars.

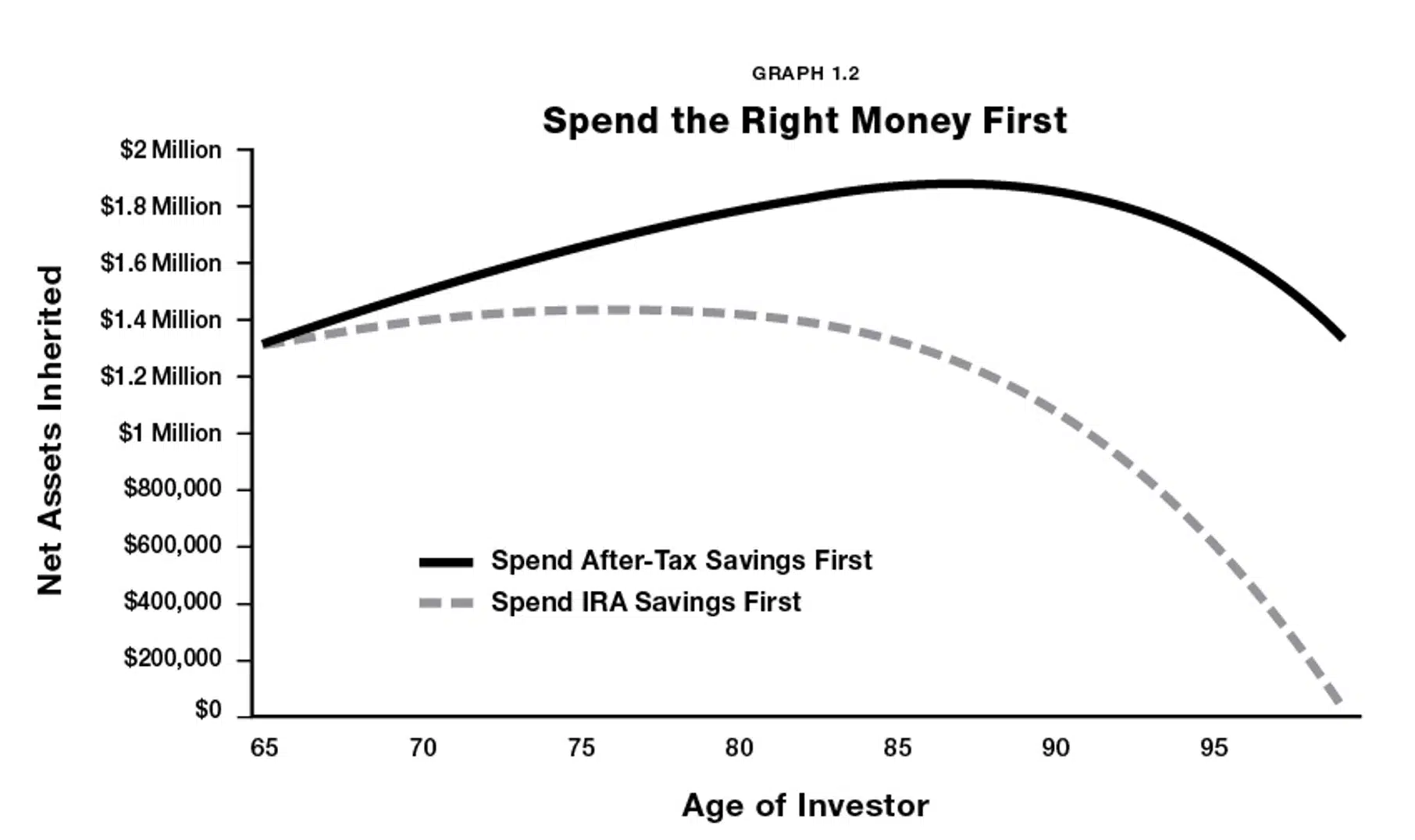

Please look at the graph that follows. Both couples start with the same amount of money in a regular brokerage account—which I refer to as after-tax dollars—and in their retirement plans. The graph below indicates, subject to exceptions, that most readers should spend their after-tax dollars first and then IRA and retirement plan dollars. The solid line shows what happens to the first couple who spend their after-tax dollars first and withdraw only the minimum from the IRA when they are required to (more on RMDs in the next section). They pay-taxes-later. The dashed line shows what happens to the second couple who spend their IRA first. They pay-taxes-now.

Graph 1.2: Spend the Right Money First

Detailed assumptions for Graph 1.2: Spend the Right Money First

- Investor retires at age 65 with $1.1 million in qualified retirement accounts and $300,000 in after-tax accounts.

- Assumes annual Social Security income of $25,000 + spousal of $12,500.

- 25% ordinary tax rates.

- Beginning annual spending of $90,000; adjusted for inflation annually by 3.5%.

- 7% rate of return.

The only difference between the dashed line and the solid line in this graph is that the first couple retained more money in the tax-deferred IRA for a longer period. Even starting at age 65, the decision to defer income taxes for as long as possible gives the first couple an extra $625,591 if the couple lives to age 87. If one of them lives longer, paying taxes later will be even more valuable to them.

Subject to exception, I generally prefer you not spend your Roth IRA dollars unless there is a compelling reason. The Roth IRA grows income tax-free for the rest of your life, your spouse’s life and for 10 years after you and your spouse are gone. In addition, there is no required minimum distribution for you or your spouse with a Roth IRA.

So, in general, the last dollars you want to spend are your Roth IRA dollars. Of course, there may be time when it makes sense to spend your Roth dollars before other retirement plan dollars if it keeps you in a lower tax bracket.

That said, subject to exceptions, you and your spouse will realize a benefit by deferring the income taxes due on your retirement plans for as long as possible and generally hold off on spending your Roth IRA. And with the SECURE Act now part of the law, your children, and grandchildren (subject to some important exceptions, which I will cover in Chapter 5) will have to pay income taxes on the Inherited Traditional IRA within 10 years of your death.

A New Wrinkle in our Bedrock Principle

Since the passage of the SECURE Act, adhering to the pay-taxes-later rule in the distribution stage might not always be the best advice. With income tax rates likely on the rise, for some professors it might make more sense to plan for a transition from the taxable world (most TIAA accounts, IRAs, retirement assets, etc.) to the tax-free world (Roth IRAs, 529 plans, life insurance, your children’s Roth IRAs, etc.). To get the best result, it is best to analyze each situation on a case-by-case basis.

In short, the SECURE Act dramatically accelerates the taxes on your retirement plan after your death. For your children, losing the lifetime stretch on an inherited retirement account can carry a huge tax burden. I will cover this idea more in Chapter 5.

One reasonable strategy for some professors with significant IRAs and retirement plans who will not likely spend all their money is to make taxable withdrawals from the retirement plan and/or IRA, pay the tax, and then gift the net proceeds. The gift could be invested in something that grows tax-free like a 529 plan, your children’s Roth IRAs, life insurance, etc. That serves the purpose of getting some money out of your estate and allows tax-free growth for your children.

As a result, for many faculty members, an earlier transition from the taxable world to the tax-free world might work better than the standard rule of “pay taxes later.”

About Your Presenter: James Lange, CPA/Attorney

Jim is the author of 10 best-selling financial books and has been quoted 37 times in The Wall Street Journal. He has published 21 articles for Forbes.com.

")

(1)")

")

")

As I have written about, this is personal to me. I was hoping that distributions from my Roth IRA and IRA would be “stretched” over the life of my daughter and maybe grandchildren. It could make a difference of well over a million dollars to my family.

As I have written about, this is personal to me. I was hoping that distributions from my Roth IRA and IRA would be “stretched” over the life of my daughter and maybe grandchildren. It could make a difference of well over a million dollars to my family. The House is scheduled to vote on Thursday, May 23, 2019, on the SECURE ACT. Then, it will be in the Senate’s court to vote on RESA. Then the House and Senate will need to reconcile the differences between the bills. Experts, including us, think a compromise will be found and that the “stretch IRA” as we know it, will be gone, dealing a severe blow to IRA and retirement plan owners who were hoping their heirs would be able to continue deferring the distributions on their inherited IRAs and retirement plans for decades.

The House is scheduled to vote on Thursday, May 23, 2019, on the SECURE ACT. Then, it will be in the Senate’s court to vote on RESA. Then the House and Senate will need to reconcile the differences between the bills. Experts, including us, think a compromise will be found and that the “stretch IRA” as we know it, will be gone, dealing a severe blow to IRA and retirement plan owners who were hoping their heirs would be able to continue deferring the distributions on their inherited IRAs and retirement plans for decades.