")

How Grandparents Can Best Provide

for Their Grandchild with a Disability

by James Lange, CPA/Attorney

Reprinted with permission of Forbes.com where Jim is a paid contributor.

I helped implement a tax saving strategy for my recently deceased father-in-law that, given reasonable assumptions, will save our family $1,178,397 in taxes over our daughter’s lifetime. To oversimplify, I redirected what would have been my wife’s $500,000 inherited IRA to our daughter's Special Needs Trust (SNT).

Many grandparents of children with disabilities can take the same tax-cutting steps we did to help protect their grandchild’s long-term financial security and independence.

Please note this strategy could also have significant benefits to grandparents who don’t have a grandchild with a disability. Grandparents with children, who are in a substantially higher tax bracket than their grandchildren, can take similar tax-cutting steps.

If you are skeptical, please note that this strategy was published and attributed to me in The Wall Street Journal on December 22, 2025 in an article by Ashlea Ebeling.

The Common Default

Most grandparents with traditional families name their spouse as the primary beneficiary of their IRA and other retirement plans. Then, typically, they name their children equally as the contingent beneficiaries of their IRAs. That means if their spouse predeceases them, their children inherit the IRAs equally. You may also see the words "per stirpes" on the beneficiary form to indicate that if one of the children predecease their parents, then the share of the predeceased child goes to the child or children of the predeceased child.

The Improvement in the Common Default

I suggest adding flexibility to the documents by including “disclaimers” (see below) and in the case of a grandchild with a disability to allow a child to “disclaim” to a SNT.

Some estate attorneys have been using variations of this disclaimer strategy for more than 30 years. The objective has always been to allow grandparents to set up a flexible estate plan that could direct at least a portion of their IRA to a grandchild or to a trust for one or more grandchildren. Over that time many IRAs were directed or disclaimed to grandchildren, saving hundreds of thousands of dollars or more in taxes.

Disclaimer Planning to a SNT

A disclaimer is a legal way to refuse an inherited IRA (or a portion of an IRA or any other asset) so it passes automatically to the next contingent beneficiary named in the beneficiary designation. You aren’t changing the beneficiary form after death, just allowing a named beneficiary to step aside in favor of a contingent beneficiary. For most traditional families, I often prefer estate plans that have a series of disclaimers built in on several levels.

Specifically in the context of this article, I am recommending you consider giving your child the choice of accepting their share of their inherited IRA or disclaiming it into the SNT for their child.

Why IRAs and Retirement Accounts Are Especially Well-Suited for a SNT

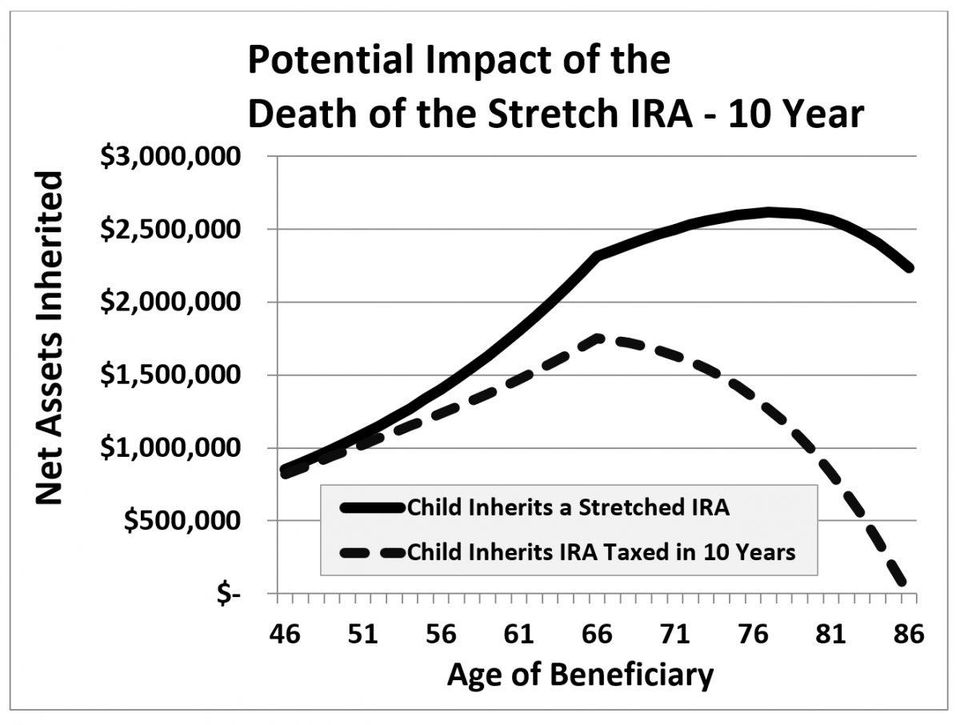

IRAs and retirement accounts are fully taxable when distributed. Under the current law known as the SECURE Act, for deaths after December 31, 2019, subject to exception, inherited IRAs must be distributed and taxed within ten years after the death of the IRA owner. This often results in massive income tax acceleration for grown children who may already be in high-income tax brackets.

However, when an inherited IRA passes directly or via disclaimer to a SNT for a beneficiary with a disability who qualifies as an Eligible Designated Beneficiary (EDB), the beneficiary can "stretch" distributions—deferring taxes—over their actuarial life expectancy. For a child who likely will need lifetime support, this difference can be life changing.

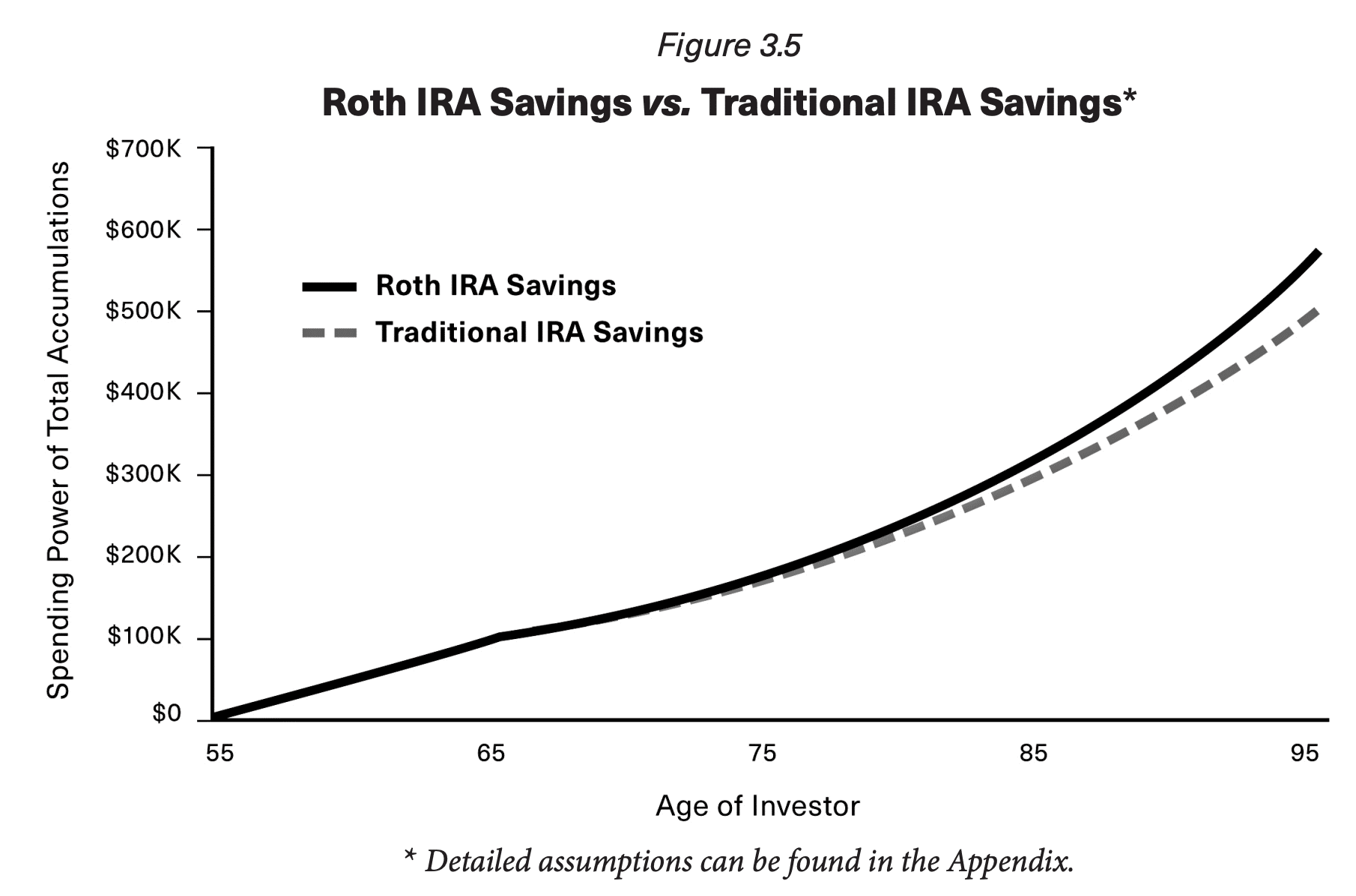

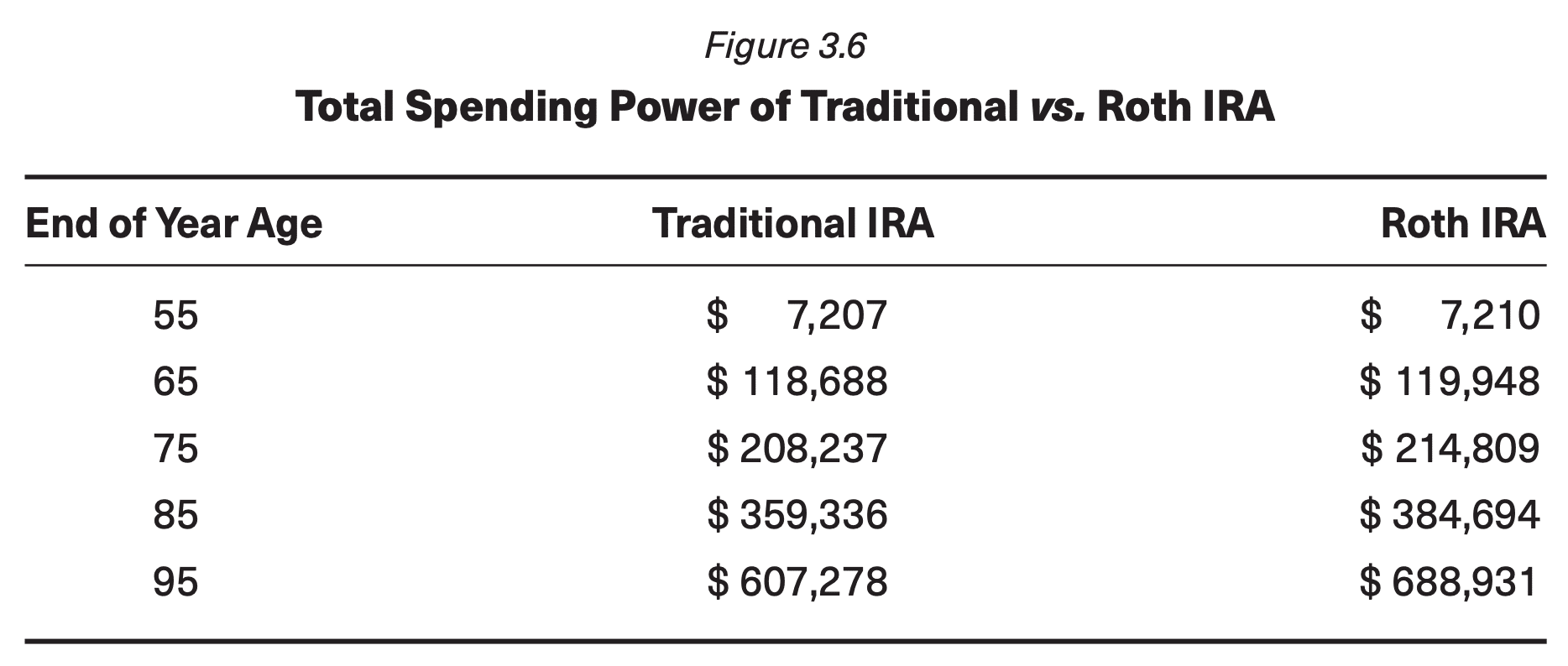

In our family's case, we benefited in two ways. First, we avoided the standard ten-year distribution of the inherited IRA rule that would have forced my wife to pay income taxes on her portion of her dad's IRA over ten years. Instead, our daughter’s trust will enjoy a 50-plus-year “stretch” based on our daughter's life expectancy. In addition, our daughter, who will receive taxable distributions from the trust will be in a lower income tax bracket than my wife and I. Combining both tax benefits with reasonable assumptions*, our daughter will enjoy $1,178,397 in additional savings over her lifetime. (Please see the graph below for a timeline of the projected benefit of the strategy we recommend.)

*Assumptions

- $500,000 inherited IRA with a 10-year stretch vs. 60-year lifetime stretch

- 6% rate of return, 3% inflation rate (net rate of return of 3% more than inflation)

- Parent vs. grandchild annual income = $150,000 vs. $18,000 SSDI (assume all after-tax income is spent by both parent and grandchild except for IRA distributions)

- Current income tax rates for federal tax purposes

- 15% tax rate on portfolio income for both parent and grandchild

- No inheritance, estate, or state income tax are included in the analysis

Note: No information provided should be construed as tax, legal or investment advice. Speak with a qualified professional prior to implementation.

This plan doesn't work nearly as well today if the grandchild doesn't have a disability, however, there is still an opportunity to use trusts to save taxes when the grandchild is not disabled but their tax rate is considerably lower than their parents’.

My strong recommendation for grandparents of a grandchild with a disability is to consider naming a properly drafted SNT as a contingent beneficiary of their IRA or retirement plan. If the grandchild doesn’t have a disability, then consider including disclaimer provisions either to a grandchild directly or a standard minor’s trust to take advantage of the grandchild’s lower tax bracket.

What Our Family Actually Did

I requested my father-in-law add a SNT for the benefit of our daughter who has a disability as the contingent beneficiary of my wife’s share of the inherited IRA. He did that. After he passed, my wife disclaimed her share of his IRA to the SNT.

With or without disclaimers, if you want to benefit a grandchild with a disability, you usually need a SNT. The SNT can offer protection when an outright inheritance to a grandchild with a disability could threaten eligibility for means-tested benefits like Supplemental Security Income (SSI) and Medicaid. In addition, it can unnecessarily cause a massive income tax acceleration.

How to Enhance This Strategy

What is better than long-term income-tax deferred investments? Long-term tax-free investments. If grandpa or grandma converts some of their IRA to a Roth and that Roth can eventually go to a SNT, the SNT will have the same “stretch” distribution pattern as a traditional IRA, but all the qualifying distributions will be tax-free.

My wife and I made a $250,000 Roth conversion in 1998. That Roth, including the growth from the time that we converted it until our death which will hopefully be a 50-year period, will eventually pass to our daughter, who will stretch that inherited Roth IRA over her lifetime. Our family might get over 90 years of tax-free growth on that Roth conversion. That Roth conversion story, which also created a million dollar plus benefit for our daughter, along with other benefits of Roth conversion planning, was published in Forbes magazine in the February 28, 2019 edition.

Warning

Drafting the trusts, implementing the disclaimers, and taking all the necessary steps to achieve the goals of this article is a minefield where one misstep can cause a massive income tax acceleration. Those considering this strategy are advised to work with a qualified estate attorney and advisor to avoid mistakes.

Furthermore, there is no rush to do anything with the inherited IRA immediately after a death. You have nine months to make a disclaimer. Don’t let the executor, the trustee, the beneficiary, or the financial institution where the money is invested do anything until you have all your ducks in a row, that is, when the strategy and the mechanics of what to do are clearly defined. I have seen a lot of wonderful disclaimer opportunities ruined because someone did something they should not have done after death.

The banker we dealt with would have made a deadly mistake that would have killed the “stretch” for our daughter had I not been so diligent to make sure everything was done right.

The Takeaway

If a family includes a grandchild with a disability, naming a SNT as a contingent beneficiary of an IRA either directly or through a disclaimer is one of the highest impact planning moves available. Converting part of that IRA to a Roth is like adding the cherry on top.

Directing IRAs or retirement accounts—or better yet Roth IRAs—to a SNT can easily save families with a $500,000 IRA or more hundreds of thousands of dollars per beneficiary (sometimes well over $1M in taxes) and provide lifetime support for a grandchild with a disability. The evidence is in the track record of families who got it right, including mine.

About Your Presenter: James Lange, CPA/Attorney

Jim is the author of 10 best-selling financial books and has been quoted 37 times in The Wall Street Journal. He has published 21 articles for Forbes.com.

As I have written about, this is personal to me. I was hoping that distributions from my Roth IRA and IRA would be “stretched” over the life of my daughter and maybe grandchildren. It could make a difference of well over a million dollars to my family.

As I have written about, this is personal to me. I was hoping that distributions from my Roth IRA and IRA would be “stretched” over the life of my daughter and maybe grandchildren. It could make a difference of well over a million dollars to my family. The House is scheduled to vote on Thursday, May 23, 2019, on the SECURE ACT. Then, it will be in the Senate’s court to vote on RESA. Then the House and Senate will need to reconcile the differences between the bills. Experts, including us, think a compromise will be found and that the “stretch IRA” as we know it, will be gone, dealing a severe blow to IRA and retirement plan owners who were hoping their heirs would be able to continue deferring the distributions on their inherited IRAs and retirement plans for decades.

The House is scheduled to vote on Thursday, May 23, 2019, on the SECURE ACT. Then, it will be in the Senate’s court to vote on RESA. Then the House and Senate will need to reconcile the differences between the bills. Experts, including us, think a compromise will be found and that the “stretch IRA” as we know it, will be gone, dealing a severe blow to IRA and retirement plan owners who were hoping their heirs would be able to continue deferring the distributions on their inherited IRAs and retirement plans for decades.